The 2026 luxury goods sector outlook from BNP Paribas is cautiously optimistic, though significant uncertainty remains. After a flat 2025, BNP Paribas Equity Research projects 6% organic sales growth for the luxury market in 2026, although visibility remains low due to macroeconomic, currency and idiosyncratic risks.

This forecast assumes some macro improvement as well as the end of the post-pandemic super-cycle normalisation and a weighted average that masks significant company-level volatility. Margins are expected to be flat after further decline in 2025 driven by FX headwinds, tariff effects and commodity pressures in the luxury industry. Our experts are most constructive on the US market, expect a gradual improvement in China, and have mixed feelings regarding Europe and the rest of the world, which still represents 50% of sector sales.

Luxury sector organic growth

Source: BNP Paribas estimates

FX headwinds and their impact on luxury margins

BNP Paribas Equity Research experts expect margins to flatten in 2026 after a slight dip in 2025. The 2025 decline stemmed from flat organic sales growth leading to continued operating expenditure deleverage, pricing broadly in line with 2024 (although mitigated by tariff impacts in the second half of the year), limited product mix effects and greater cost control. Hedging has cushioned most FX headwinds, though some firms will feel negative currency impacts sooner.

Looking to 2026, flat margins despite an estimated 6% average organic sales growth reflect FX headwinds hitting margins with a lag depending on hedging and modest operating leverage for firms outperforming the 6% sector average. Meanwhile, the effects of tariffs will be felt over the full year versus H2 in 2025, and some groups will be hampered by commodities impacts.

❝ Currency headwinds will cut 2026 revenue growth to 4% (from 6%) and put pressure on profitability, unlike 2025, when a -3% FX hit on revenue was fully hedged. The hedges covering 2025’s adverse currency impact end in 2026. ❞

US luxury market: a growth engine in 2026

Our experts point to the US as the only region with positive short and medium-term catalysts. Accounting for 23% of global sector sales, the market now ranks first in growth contribution in the medium term, alongside China and remains under-penetrated for luxury.

After the post-Covid super-cycle and subsequent digestion, sales reaccelerated in the second part of 2025, driven further by the “AI frenzy” and wealth effects from strong equity and cryptocurrency markets. According to BNP Paribas Equity Research experts, the US Luxury market has now probably reached the end of this phase, with prices increasing less, consumers getting used to higher pricing, and some consumers perhaps ready to resume spending after a recent pause.

❝ On US Luxury, US investors focus on the significant store expansion capex still planned in 2026, supporting our thesis this market is still under-penetrated; however, since this market is the most correlated to equities, we came across some investors who questioned the sustainability of the US equity boom and AI frenzy. ❞

China luxury outlook 2026: stabilising macroeconomic indicators

Our experts are constructive on China, expecting the market to grow 6% in 2026, with a 10% CAGR from 2027 to 2031, due to a modest and gradual improvement in Chinese consumer sentiment as shown by macroeconomic indicators, limited structural changes and a so-called “affluent” population of around 25 million expected to resume spending as a result of stronger financial markets and AI-related jobs after several years of continued wealth creation combined with high savings rates. Our experts expect China’s GDP growth to be around 5% in 2026. The property market is stabilising, with daily property sales showing signs of recovery, although still below pre-Covid levels.

China accounts for 25% of global luxury sales, making it a crucial market for brands, which have been adapting through effective product activations, marketing campaigns, store network optimisation, and consumers responding well to these brand-led initiatives.

❝ In a way, Chinese Luxury [is] finally succumbing to several years of economic worries, notably in terms of real estate and job markets – in our view simply marked a ‘coming of age’ of that market, ie starting to behave like

other luxury markets. ❞

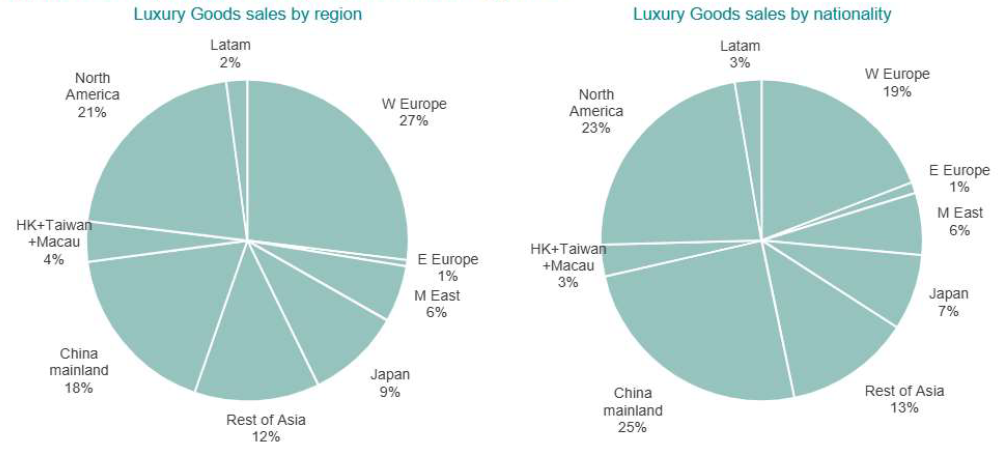

Luxury goods sector sales by region & nationality, 2025 estimate

Source: BNP Paribas estimates

Rest of world demand fuels 50% of luxury growth

After China and the US, the rest of the world still accounts for nearly half of global luxury demand and displays significant polarisation, with brand desirability the most important factor. European demand is robust, with brands elevating their service levels to local clientele.

❝ Nationalities outside of the Top 4 – US, Chinese, European, Japanese – together account for 20-25% of global sales for Luxury brands. These “other” nationalities of consumers should not be forgotten (we call them the ‘silent quarter’). ❞

The Middle East stands out as a bright spot, adding retail space with strong luxury demand – even weak global brands show minimal decline here. However, political stability and oil prices are both vital to sustained spending. High-end brands are outperforming in Japan, while the rest of Asia remains difficult to read. Structural challenges in India remain, and markets such as LatAm, Africa and Indonesia remain dormant with negligible short‑term impact.

For more details on BNP Paribas Equity Research, please visit:

BNP Paribas does not consider this content to be “Research” as defined under the MiFID II unbundling rules. If you are subject to inducement and unbundling rules, you should consider making your own assessment as to the characterisation of this content. Legal notice for marketing documents, referencing to whom this communication is directed.