The European Commission unveiled its strategy for a “Savings and Investments Union” (SIEU) recently, as the bloc addresses the need to find the necessary funding for the massive investments required for the twin transition – energy and technological. Securitisation is an essential component, with the Commission proposing new measures to boost securitisation in the European Union, while preserving financial stability.

In a recent publication, Laurent Quignon from BNP Paribas’ Economic Research department, explains that these measures form a strong foundation to revive the securitisation market, and looks to further steps that could be taken.

❝ The capital requirements imposed on securitisations must be aligned with those relating to other assets of comparable risk if we are to ensure investor interest and fully unlock this market. ❞

Unlocking the full benefits of securitisation

Laurent Quignon highlights the role of securitisation as a powerful tool for improving market efficiency, savings allocation and financing the economy, with a range of benefits:

- diversification and enhanced risk distribution;

- increased liquidity and thus supporting the exchange and valuation of the assets;

- greater adaptation to investors’ risk/return requirements.

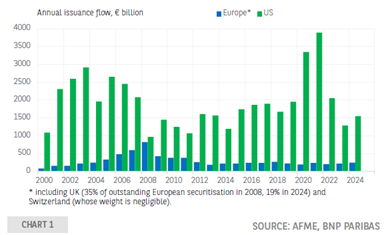

Yet despite the overhaul of the EU securitisation framework since 2019 to promote sound securitisation, issuance remains low, particularly compared with the United States.

Securitisation issuance compared between Europe and the United States

A new range of necessary measures mark step in right direction

The European Commission’s recently announced reform of the legislative and regulatory framework for securitisation is designed to address this situation, and Laurent Quignon identifies a number of impacts:

- On the supply side, the proposal improves prudential calibration, by reducing current capital charges on one hand, and introducing risk sensitivity on the securitisation tranches retained by banks on the other. This is designed to have a positive effect on the volume of securitisation transactions issued by banks.

- On the demand side, the proposal seeks to avoid risks being re-injected into the banking system so does not substantially alter current treatment for exposures of banks acting as investors.

- The proposal also simplifies due diligence requirements for investors. At the same time, the Commission has launched a consultation to amend delegated regulation on the liquidity coverage ratio to make securitisation exposures eligible for the liquidity coverage ratio numerator.

Greater capital alignment required

While the economic impact of these new proposed measures is difficult to assess, Laurent Quignon concludes that the proposal is a step in the right direction. He highlights that bringing capital requirements more into line with risk could further broaden the scope of securitisable loans, particularly for relatively high-risk loans and boost issuance volumes in these segments.

In light of the imbalance in the prudential treatment for securitisation compared with asset classes with a similar risk profile, he concludes that the draft amendment to Solvency II delegated regulation, which aims to “take better account of the real risks of securitisation and eliminate the unnecessary prudential costs borne by insurers when they invest in securitisations”, will be decisive in reducing this disparity and revitalising this market.

Visit the Economic Research – BNP Paribas portal for more information

Securitisation, a longstanding instrument

Securitisation, in its so-called “cash” version, involves banks grouping loans into relatively homogenous “packages”, then transferring them to a special purpose vehicle (SPV), which in turn transforms them into more liquid securities by issuing units in the SPV. Some of these securities are kept on the balance sheet of the originating bank, while others are placed on the market with institutional investors and acquired by other banks. The equity freed up on the balance sheet of the originating bank as a result of the sale of transferred loans can be reallocated to financing new projects. Today, in the European Union, a large proportion of securitisations are synthetic, meaning that the risk is transferred, but the underlying asset remains on the balance sheet of the originating bank.