Given that transport accounts for around 30% of the European Union’s CO2 emissions, it’s no surprise that issues related to Environment, Social and Governance (ESG) are an increasingly central topic for the automotive industry. As pressure to reduce carbon emissions across the industry intensifies, especially with Scope 2 and 3 expected to take centre stage in the sustainability debate post COP26, suppliers are increasingly expected to contribute to this reduction.

In June, for example, it was reported that Toyota had asked its parts suppliers to reduce carbon emissions, initially by 3% – while BMW last year said that suppliers’ carbon footprints would be a key factor in the tender process. Other notable developments include the recent publication of a new guidance document by the Suppliers Partnership for the Environment, Key KPIs to Track and Reduce CO2 Among Automotive Suppliers.

Against this backdrop, BNP Paribas and Boston Consulting Group (BCG) released a joint study earlier this year focusing on sustainability and ESG in the German automotive supplier industry. The study, which was published in August, includes some significant insights from 24 automotive suppliers in Germany which together represent more than 50% of the total turnover of German suppliers.

Green and sustainable financing has matured considerably in recent years (…) However, not all suppliers have fully recognised the benefits of green financing at this stage.

Reinhard Kuehn, Co-Head Automotive and Mobility EMEA, BNP Paribas

The story so far

The survey reveals that while around 80% of the suppliers surveyed regard ESG as a top priority, over 70% have not yet started to implement specific measures to address this issue. And of the suppliers that are implementing measures, most are larger and mid-sized companies.

There are a number of reasons for this lack of action. The top obstacle, cited by around 40% of respondents, was the internal implementation effort, with responses citing the difficulties involved in getting employees on board, as well as challenges in convincing the organisation about the need for the additional workload. Other hurdles included increased costs (20%), dynamically changing requirements, such as customer and regulatory requirements (20%), and the implementation of ESG measures in the supply chain (15%).

A further issue identified by the report is that while 87% of suppliers are setting sustainability targets, or are planning to do so in the next two years, less than half are currently tying their performance and incentives schemes to sustainability. As such, this is something of a missed opportunity to incentivise employees to achieve their sustainability targets.

ESG ratings represent another area of untapped potential. The survey found that over 85% of suppliers are not actively engaging with ESG rating agencies, meaning that opportunities for improvement are being missed. The reasons for this included a lack of financial resources, limited understanding of the topic, and a lack of global coherence where regulations are concerned. However, as the report notes, working with ESG rating agencies provides a considerable opportunity for suppliers to improve their ESG ratings.

CO2 reduction challenges

The importance of fulfilling CO2-related targets in a timely way was highlighted by the survey, with two-thirds of new business depending on the fulfilment of mandatory CO2-related requirements. However, suppliers face numerous challenges when it comes to implementing measures to achieve a reduction in CO2: 80% noted that OEMs are not willing to pay for these efforts, with only 46% saying they were able to pass on costs and maintain their margins. But for suppliers with a mature sustainability agenda, the picture was somewhat different, with two thirds saying they were able to pass on their costs.

Other challenges for CO2 reduction included a lack of transparency on Scope 3 baselines and measures, a lack of cost transparency, high costs, and a lack of knowledge and talent.

Harnessing green financing

Reinhard Kuehn, Co-Head Automotive and Mobility EMEA at BNP Paribas explained: “Green and sustainable financing has matured considerably in recent years, with the established reputational benefits accompanied by other advantages such as the ability to attract new investors and access lower cost funding. However, not all suppliers have fully recognised the benefits of green financing at this stage.”

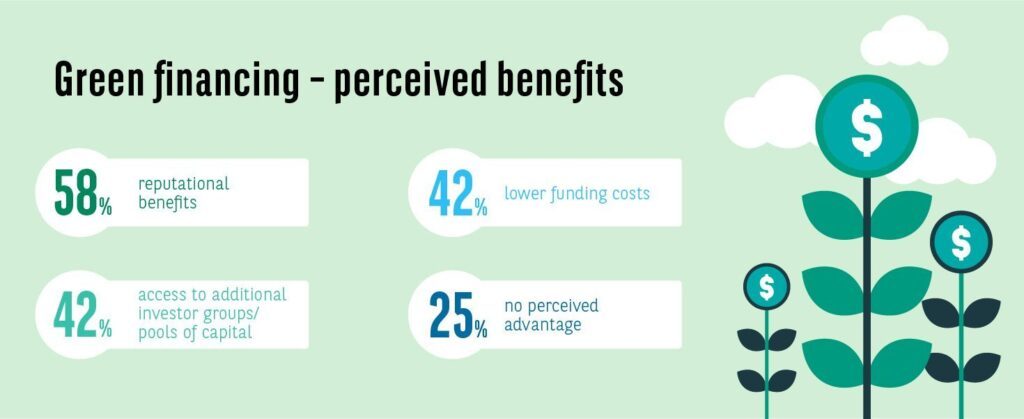

Fifty-eight percent cited reputational benefits, followed by access to additional investor groups and pools of capital (42%) and lower funding costs (42%). But a quarter of the survey’s respondents said green financing has no perceived advantage.

Where specific instruments are concerned, the most relevant instruments were identified as green/sustainability linked loans (cited as relevant by 55% of respondents), and green or sustainable bonds (46%).

Respondents from public companies were also asked how frequently ESG is a topic during investor calls. The results suggested that this varies considerably between companies: around 45% said that ESG is addressed on a monthly basis, while a third of respondents said it is only addressed annually.

Steps to success

Finally, the report identifies six main steps that automotive suppliers can take to benefit from ESG:

- Create transparency – assess key areas of strength, identify group-wide material issues and understand peers’ approach.

- Define targets – define relevant ESG indicators, compare asset performance to industry peers and develop a sustainability strategy.

- Create roadmap – build a business case and define a prioritised measure roadmap.

- Set up steering – define KPIs for performance assessment and reporting; outline a lean and efficient sustainability operating model.

- Communicate externally – align plans with all relevant stakeholders; define ecosystem strategy, including communication and policy shaping.

- Activate benefits – mitigate risk, access green financing and build a competitive advantage for customers through ESG differentiation.