Agnes Gourc, Head of Sustainable Capital Markets at BNP Paribas CIB, looks into their specific characteristics and their benefits for issuers and investors.

What are the latest trends in the social bond market?

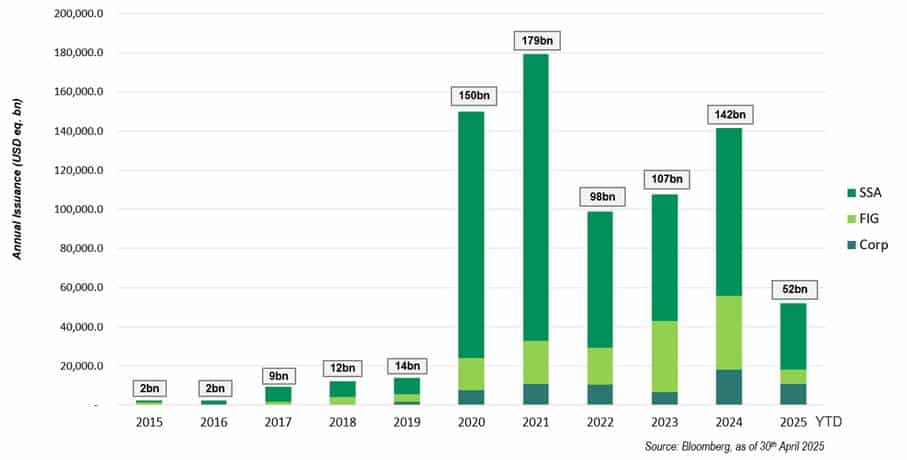

Social bonds are not a new thing, amounting to as much as USD719 billion issued globally at the end of 2024. Government-related agencies and financial institutions were the first to issue social bonds around twenty years ago, notably with IFFIm bonds supporting the financing of global vaccine programmes. These instruments significantly gained in popularity, first with the development of the ICMA Social Principles in 2016, with a significant jump in issuances in 2020 and 2021 to help fund the recovery efforts during the Covid19 pandemic.

Social bonds by issuer type

Social bond issuance jumped ~30% worldwide in 2024 to USD142 billion, compared to the previous year, and already stands at USD52 billion by the end of April this year.

Investing in social bonds is one way for investors to diversify their portfolios across different sectors and geographies while aligning with sustainability goals.

Moreover, social bonds are also part of a broader trend towards thematic investment, with investors increasingly seeking impact, as evidenced by our last thematics barometer whereby 71% of investors surveyed ranked achieving positive impact and contributing to sustainable outcomes as their leading objective for their thematic allocations.

BNP Paribas is active in sustainability globally, and societal resilience is a topic that emerges regularly in our dialogue with clients. We draw on our extensive sustainable platform to develop solutions that align with our issuer clients’ needs and our investor clients’ priorities.

How do social bonds enable impact?

Social bonds are used to finance or refinance new and existing projects that address or mitigate specific social issues and seek to promote positive social outcomes. They can play a key role in driving progress towards the United Nations’ Sustainable Development Goals with various benefits across sectors such as affordable housing, healthcare, education, access to essential services such as power and electricity, among others.

Importantly, these debt instruments require issuers to demonstrate specific and measurable impact, with proceeds earmarked for social projects. The most common projects tend to involve affordable basic infrastructure – provision of clean drinking water, sewers, sanitation, transport, energy for example – access to essential services, affordable housing, Just Transition, food security and sustainable food systems. Social bonds can also support socioeconomic advancement goals and empowerment of small and medium-sized businesses that lack access to finance.

Issuers must ensure that the funds raised are directed towards projects where the impact can be quantifiably and effectively measured. This transparency is a key factor for investors and the issuer must provide allocation and impact reports.

What are the latest innovations in this space?

There have been some interesting innovations over the past years. Starting with the African Development Bank’s (AfDB) USD750 million global benchmark perpetual sustainable hybrid bond last year, which was the first ever hybrid capital transaction from a multilateral development bank. Under a new Sustainable Bond Framework, the issuer aims to finance a combined portfolio of eligible green and social projects, including access to basic infrastructure and essential services, as well as food security and socioeconomic advancement and empowerment. Additionally, with 100% of the notional amount recognised as equity by the rating agencies, any hybrid capital bond by the AfDB is expected to enable at least USD2 of additional lending activity for every USD1 raised. BNP Paribas supported AfDB as joint structuring agent, joint global coordinator and joint bookrunner.

Banks have also a critical role to play in mobilising funding towards socially sound and sustainable projects that achieve greater social benefits. BNP Paribas launched its Social Bond Framework in late 2022 in line with the ICMA Social Bond principles. Assets are selected by BNP Paribas’ Social Bond Committee, sourced from the various eligible categories, in line with our CSR policies and applicable regulatory requirements, as well as voluntary filters. Proceeds are used to finance or refinance assets and projects that deliver positive social impact, including access to employment, equal opportunities, access to housing, education and healthcare.

This Framework highlights the social asset origination of BNP Paribas’ commercial banks and broader CPBS division, initially leveraging only French commercial banks’ assets but gradually extending to the rest of Europe. Around EUR1.6 billion has been issued under the Framework so far since the inaugural structured social index-linked bond, structured by the Global Markets business of BNP Paribas CIB and invested in by the insurer BNP Paribas Cardif. This bond also incorporated a social donations mechanism, whereby part of the total amount invested is donated to associations supported by the BNP Paribas Group.

What could advance the social bond market further?

Unlike for green bonds where proceeds are typically used to support climate mitigation and adaptation, with impact indicators often measurable in terms of avoided emissions, the impact of social bonds can be more difficult to assess given the diversity of the social projects funded and the fact that impact metrics differ from one social goal to another. While investors appreciate specific impact metrics that reflect the efficiency of the funds deployed, they also need a single metric that can be reported across the portfolio, such as the number of beneficiaries.

In this context, the Social Bond Principles (SBP) administered by the International Capital Market Association (ICMA) have supported the social bond market by promoting transparency and disclosure. Last updated as of June 2023, these principles are voluntary process guidelines that promote integrity in the development of the social bond market, by clarifying the approach for their issuance. They recommend a clear process and disclosure for issuers, which the rest of the ecosystem – investors, banks, underwriters, arrangers, placement agents and others – may use to understand the characteristics of any given social bond.