Key takeaways

- Semiconductor market growth in 2026 and 2027 is driven primarily by higher prices rather than rising unit volumes.

- Industrial semiconductors have entered a broad restocking cycle after a prolonged inventory correction.

- Automotive semiconductor demand remains weak, with recovery likely delayed to 2027.

- Artificial intelligence is a key structural growth driver, supported by sustained hyperscaler investment.

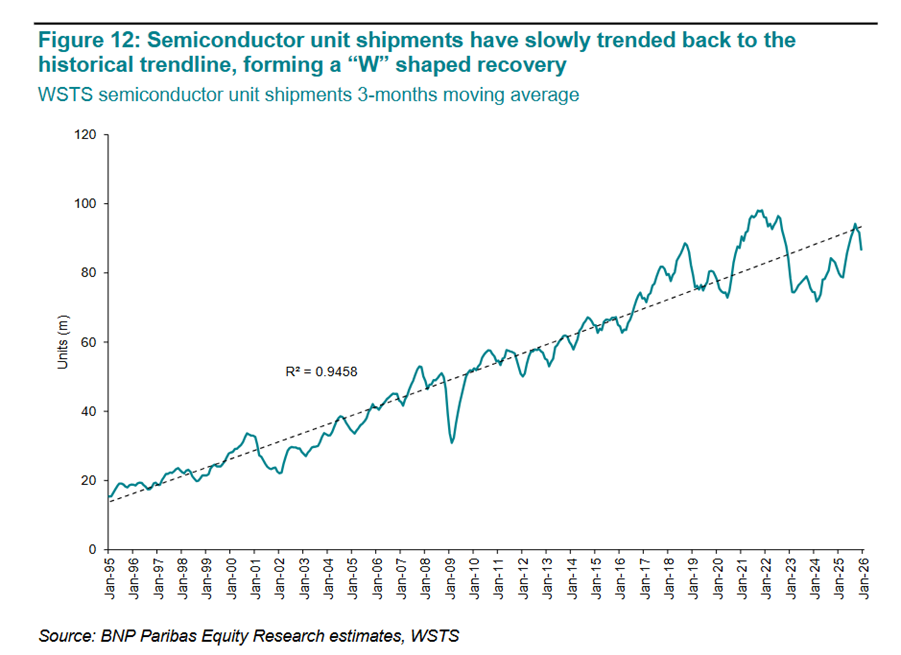

According to recent research from BNP Paribas Equity Research experts, the recovery in Semiconductors continues with units trending back to the historical trendline. The recovery since the February 24 trough has been driven by AI. In analog, early signs of recovery are emerging but unevenly.

Artificial intelligence also driving an uptick

According to BNP Paribas Equity Research, 2025 was all about AI and 2026 will be again, with AI/HPC remaining the main driver for the semi and equipment industry. AI is now available on many devices and continues to boost the sector. Major AI players are optimistic about their upcoming projects and their ability to capture market growth and market share. Robotics is a future strategic market for semiconductors, but it still needs a catalyst to drive mass adoption. Meanwhile if Agentic AI takes off, this could represent upside and trigger further investments, benefiting the sector.

Equity Research experts note that AI investments require physical infrastructure investment, as this is where the biggest gating factors increasingly are, whether chips or energy-related physical assets. The European tech hardware sector is mostly exposed to AI data centre investments through the semicap sub-sector.

❝ AI hyperscaler capex remains the main driver of European tech hardware revenue growth, both for equipment stocks and semicap. AI hyperscaler capex drives chip spend which in turn drives investments into fab capacity and ultimately drives equipment spend. ❞

Looking forward

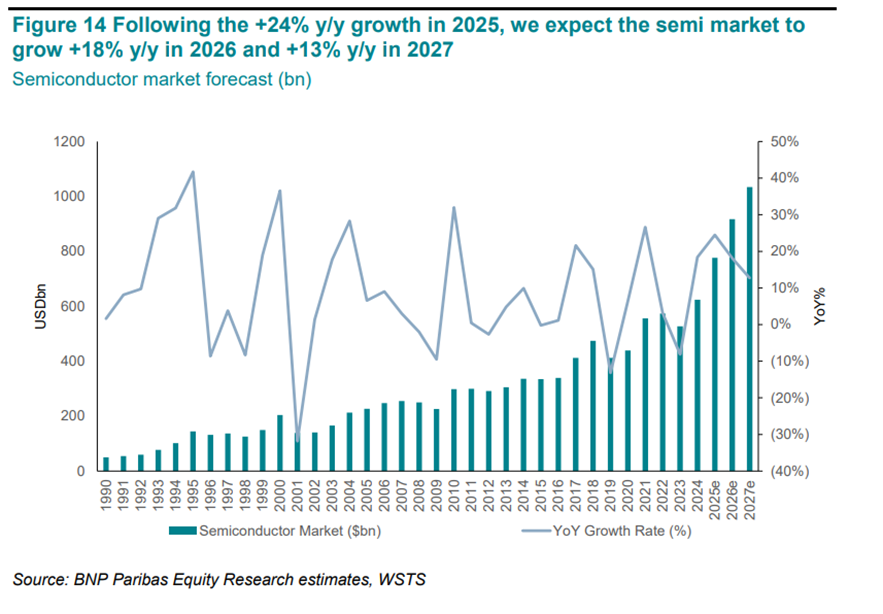

The global semiconductor market is expected to grow by 18% to nearly USD917 billion in 2026 and a further 13% to USD1 trillion by 2027 (ahead of prior expectations of 2030), supported by a significant acceleration in artificial intelligence (AI) among other factors, according to BNP Paribas Equity Research experts.

In this context, semiconductor market growth in 2026 and 2027 should mainly be driven by higher average selling prices (ASPs), and less so by an increase in unit sales.

Analog rebound: signs of recovery

The analog semiconductor market, estimated to be worth USD80-90 billion in 2024-2025, is comprised of 40% general-purpose analog chips and 60% application-specific analog chips. After a period of rapid growth following the COVID-19 pandemic, the market experienced a multi-year decline from 2023 to 2025 due to weak demand and inventory depletion.

The automotive and industrial sectors remain the primary end markets for these semiconductors, with EVs acting as the main driver of analog chip demand in automotive, highlight BNP Paribas experts.

After doubts about a rebound in 2023 and 2024, signs of a broader recovery are now emerging.

Industrial semiconductors restocking dynamics

Against this backdrop, they point to a broad-based restocking cycle under way in industrial semiconductors across technologies and geographies, as inventories grow from a very low level.

❝ Our feedback from recent industry conversations is that a restocking cycle is under way in industrial semiconductors. Nine quarters post the Q3 23 analog peak and painful inventory correction, inventories are too low and need to be restocked. ❞

Nine quarters post the Q3 23 analog peak and significant inventory correction, inventories are too low and need to be restocked say our BNP Paribas Equity analysts. A restocking cycle typically takes a few quarters to complete and is likely to drive above seasonal growth. This is also a leading indicator of industrial customers feeling better about H2 demand, supportive to the broader industrial space. Our analysts believe this restocking is broad-based across technologies and geographies.

Automotive semiconductors still in the doldrums

By contrast, automotive semiconductor demand remains uncertain, with no incremental change in either direction. While inventories are at low levels, Auto customers do not yet have the business confidence to undertake restocking.

The recovery for automotive semiconductors is only expected in 2027, but analysts underscore ongoing uncertainties particularly on China regarding competition and manufacturing localisation.

Consumer: low end demand destruction

On the consumer side, the environment is expected to be challenging in 2026, particularly for the low end across PC and smartphones, due to increasing costs and supply constraints (particularly in memory), which are expected to persist until 2027.

Read the full reports here and here, and 2026 key themes here

(For Institutional Clients only)

For Institutional Clients only – For more details on BNP Paribas Equity Research, please visit:

Cash Equities | Global Markets

BNP Paribas does not consider this content to be “Research” as defined under the MiFID II unbundling rules. If you are subject to inducement and unbundling rules, you should consider making your own assessment as to the characterisation of this content. Legal notice for marketing documents, referencing to whom this communication is directed.