Having consistently dropped for a long spell, real long-term interest rates have changed course in advanced economies in recent years. Will this uptrend continue?

In a recent publication, William De Vijlder, Economic advisor of the general management at BNP Paribas, looks at how real long-term interest rates have risen in recent years and explores how far they could go, particularly in the US given the central role of the country’s interest rates for the global economy.

Movement not over yet

According to William De Vijlder, the prospect of growing private and public sector financing is leading to concerns that the trend towards rising long-term rates may not be over. He notes that long-run momentum in long-term interest rates is fuelled on the one hand by economic growth and demographic factors, which are expected to continue exerting downward pressure, and on the other hand by massive financing needs, projected to create upward pressure.

While this latter impact should be rather limited and is already partly priced in, William De Vijlder points to the need for caution: a lasting rise in long-term rates requires greater government efforts to improve the primary balance in countries where the public debt ratio is growing.

❝ Real long-term interest rates have seen a reset in recent years that is probably incomplete, thus leaving further upside for bond yields, given the scale of the future public and private sector financing needs. With this in mind, testing resilience to positive interest rate shocks is critically important. ❞

A crucial economic variable

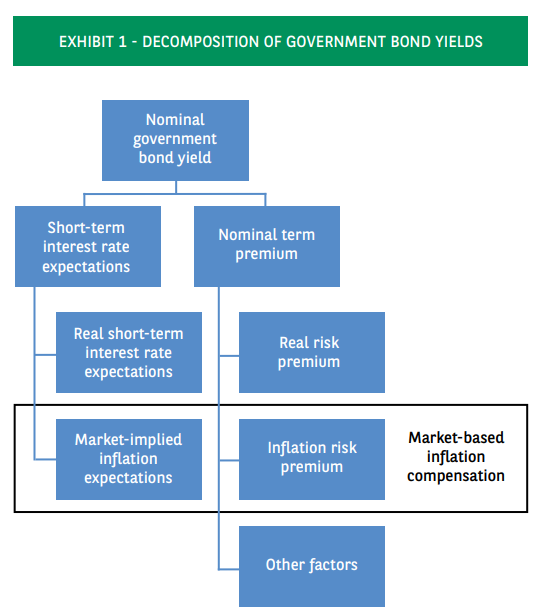

Higher interest rates impact the economy through factors such as the cost of and access to financing, effects on asset valuations, the value of loan collateral, and investor risk appetite. William De Vijlder considers the importance of understanding these determinants, and looks ahead to the long-term outlook for neutral interest rates (the real rate of interest with a shorter-run focus through its role as a reference point for monetary policy), the nominal neutral rate (adding a layer of target inflation), and the natural rate, obtained by adding a normal term premium to the nominal neutral rate. He explores the challenges in determining these rates, the factors that influence them and how they contribute to government bond yields.

Four key points to bear in mind

While acknowledging that predicting interest rate trends is challenging due to multiple factors driving the equilibrium value of short-term interest rates and the term premium, as well as markets’ difficulty in pricing in the various elements, William De Vijlder identifies four key conclusions.

Firstly, in a qualitative analysis, most factors suggest downward pressure on long-term interest rates in the future, but expected trends in financing needs (public debt and private and public investment needs) should exert upward pressure.

Then from a quantitative analysis standpoint, he notes that most models point to an expected impact on global real long-term rates by 2030 of between -19 bps and +38 bps.

Thirdly, demographic factors (life expectancy and working-age population growth) are expected to continue exerting downward pressure on long-term interest rates, according to William De Vijlder. Meanwhile investments from the private sector (energy and digital transition, AI investments) and the public sector (demands from education, healthcare, pensions, R&D, climate change and defence) are likely to exert upward pressure, although the impact should remain relatively limited.

Lastly, he advises that there is no room for complacency: a lasting increase in long-term rates requires more government efforts to improve the primary balance in countries with a growing public debt ratio. He concludes that there is a real possibility that markets are not fully pricing in upside risks to long-term interest rates in light of uncertainty on long-horizon forecasts.

For more information, please visit