Key takeaways

- Customer satisfaction is improving, and happier customers are often willing to pay more.

- Fibre-to-the-Home (FTTH) is a key driver of improved satisfaction.

- M&A activity in Europe is expected to remain market‑specific, driven by consolidation to support market repair.

Telecommunications are the backbone of the digital economy. According to the ITU, in 2025 around six billion people, or about three quarters of the world’s population, used the internet, up from a revised estimate of 5.8 billion in 2024. Mobile data traffic has surged globally over the past decade, driven by rising smartphone adoption and video consumption.

Growth is expected to continue as social media use increases, and AI-generated content expands. According to BNP Paribas Equity Research, European and North American smartphone adoption is projected to reach 91% and 90% respectively by 2030. Globally, smartphones accounted for 80% of mobile connections in 2024 and are likely to increase to 91% by 2030.

A number of key trends are set to shape this future. BNP Paribas Equity Research identifies customer satisfaction, technology such as fibre, market structure and pricing, consolidation and digitalisation as some of the main current debates in the industry, and looks to the perspectives worldwide.

Improving customer satisfaction – will pricing power follow?

Customer satisfaction has been rising again in 2026, according to BNP Paribas Equity Research, and NPS rose across most markets, notably in broadband, where the broader rollout of fibre is the key driver. According to analysts, consumer sentiment is a leading indicator for sustainable revenue and pricing power in telecoms, with higher customer satisfaction boosting willingness to pay more for services, supporting stronger pricing prospects, particularly if market consolidation materialises.

❝ Customers are happier with their telco services and happier customers are often willing to pay more. This bodes well for telco pricing, if and when consolidation occurs. ❞

Price sensitivity – is it decreasing?

BNP Paribas Equity Research notes that European consumers are becoming less price‑focused on broadband, where fibre rollouts have lifted network quality more sharply than in mobile. The shift toward speed, reliability and content has softened price pressure and reinforced the perception of “good value for money” after many years of deflationary front‑book pricing. Mobile price sensitivity, by contrast, has increased slightly.

Is customer satisfaction the driver for lower churn?

Customer satisfaction has rebounded strongly in 2026, driving a decline in churn across both fixed and particularly mobile services. Equity Research analysts point to higher NPS and improved perceptions of network quality, reinforcing the connection between service quality, customer stability and more sustainable revenue pools.

What do customers really want?

While aggregate ‘upsell’ potential remains limited at the European level, consumers show a clear preference to spend incremental income on new mobile handsets rather than higher tariffs, according to BNP Paribas Equity Research. This reflects renewed interest in device upgrades, with service upselling proving more market‑specific and dependent on consolidation dynamics.

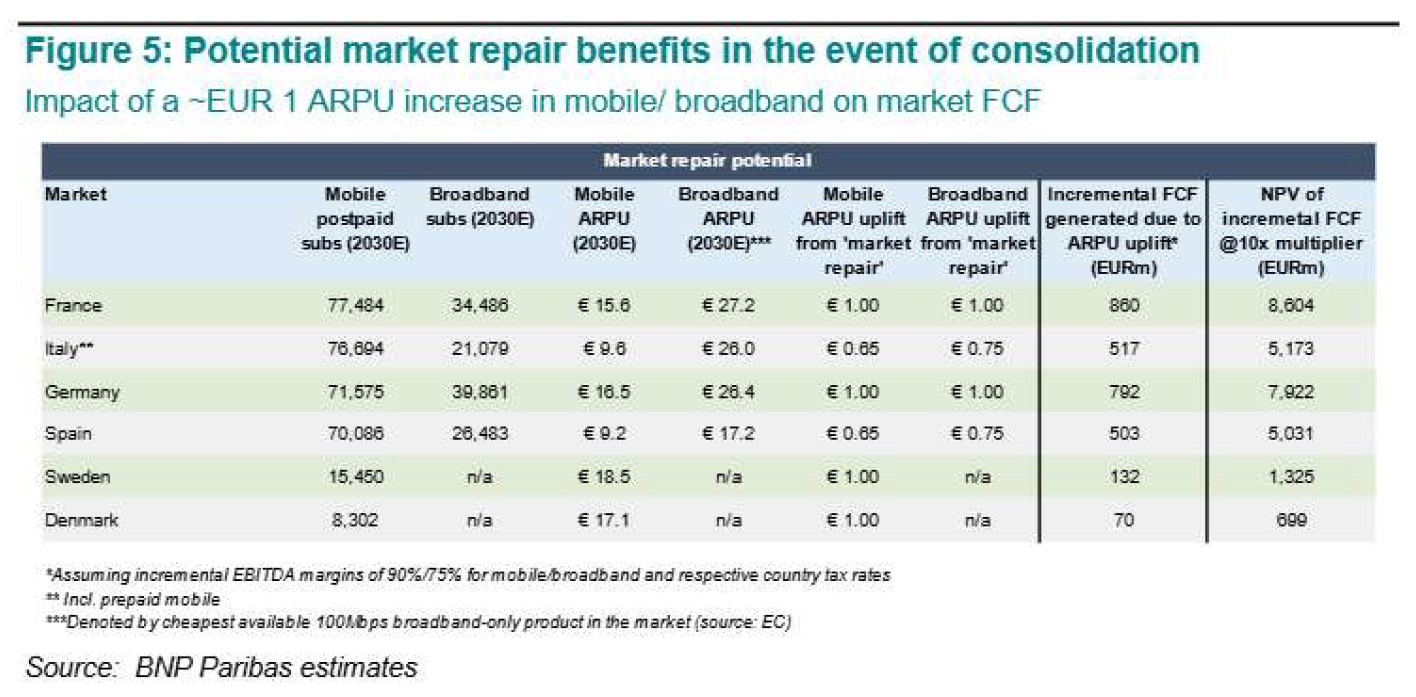

How can consolidation unlock market repair?

With opportunities identified across Europe, BNP Paribas Equity Research analysts note that in-market consolidation remains a key focus as investors are looking at the cost and long-term investment synergies and potential upside. They point to variations in market repair opportunities by market and country – price normalisation resulting from reduced competitive intensity after in‑market consolidation – with those where competition is currently high offering the greatest scope for these benefits.

❝ With a happier customer base across most geographies, there is a solid platform for ‘market repair’ in several markets which could see consolidation in the medium term. ❞

Cable versus fibre: which is the winner?

The competition between cable and fibre is central to understanding the next wave of growth. BNP Paribas Equity Research comments that customer sentiment has shifted decisively toward fibre. Equity analysts note that fibre’s technical advantages such as higher speeds, lower operating costs and greater scalability lead to superior customer metrics. Fibre is no longer a niche premium offering, but rather technology that delivers the best customer sentiment and operational efficiency. It therefore raises questions about the long‑term sustainability of cable‑only strategies.

US and Europe: two models, two different challenges

BNP Paribas Equity Research views the US telecom market as highly consolidated, with a few national players competing on price, network quality and customer experience, compared to Europe’s fragmented landscape, where consolidation could repair the market, offering better pricing discipline and more sustainable economics, especially as fibre lifts customer satisfaction and lowers churn. Sweden, Germany and the UK show improving fixed and mobile performance, while Switzerland, Finland and Belgium rank in the lower half across both segments, and other markets show mixed performance. The US, on the other hand, is in the process of fragmenting, with increasing competition from fibre, fixed wireless access and satellite – this is leading to a deterioration in the pricing environment, depressing returns for all.

❝ The US market is in flux: the last year has seen new plans, price locks, convergent offers, price cuts and more. ❞

Looking to the future

The telecoms sector’s trajectory will be shaped by four forces according to BNP Paribas Equity Research: the speed and reach of fibre rollouts, evolving ownership, financial headwinds, consolidation and the future competitive landscape.

STAMP 2026 is BNP Paribas Equity Research’s latest proprietary consumer survey covering more than 20,000 telecom users in Europe, Brazil and the US. It provides a forward‑looking view of how shifting customer sentiment impacts competitive positioning, pricing power, consolidation prospects and technology investment. This year’s results point to happier customers across Europe, probably reflecting improved network quality (more so in fixed line than mobile), and consumers getting good ‘value for money’. At a European aggregate level there is limited evidence yet that this is translating into a clear ‘upsell’ opportunity – but this varies by market.

The 1, 3 and 5 Year View: Picking up a better signal

US Cable: A fight on all fronts

For Institutional clients only

For Institutional Clients only – For more details on BNP Paribas Equity Research, please visit:

Cash Equities | Global Markets

BNP Paribas does not consider this content to be “Research” as defined under the MiFID II unbundling rules. If you are subject to inducement and unbundling rules, you should consider making your own assessment as to the characterisation of this content. Legal notice for marketing documents, referencing to whom this communication is directed.