The US dollar has been the unparalleled dominant currency at the centre of the international monetary and financial system since World War II ended 80 years ago and the Bretton Woods system was also established. Questions have arisen on this dominance from time to time, but the answer was always that nothing is going to change.

BNP Paribas’ Chief Economist Isabelle Mateos y Lago explains in a recent publication why this time feels different.

❝ This time feels different. In particular, financial markets’ reaction to the “Liberation Day” tariff announcements, whereby the dollar and US Treasuries sold off instead of being bought as the safe haven of last resort like in all previous crises. But it would be premature to call the end of dollar dominance. ❞

What is different this time?

Isabelle Mateos y Lago singles out five main reasons why the current situation diverges from the past.

First geopolitics: in the 1970s, the largest reserve holders and financial centres were all firmly part of the US-dominated Western block in the Cold War. This is no longer the case (1).

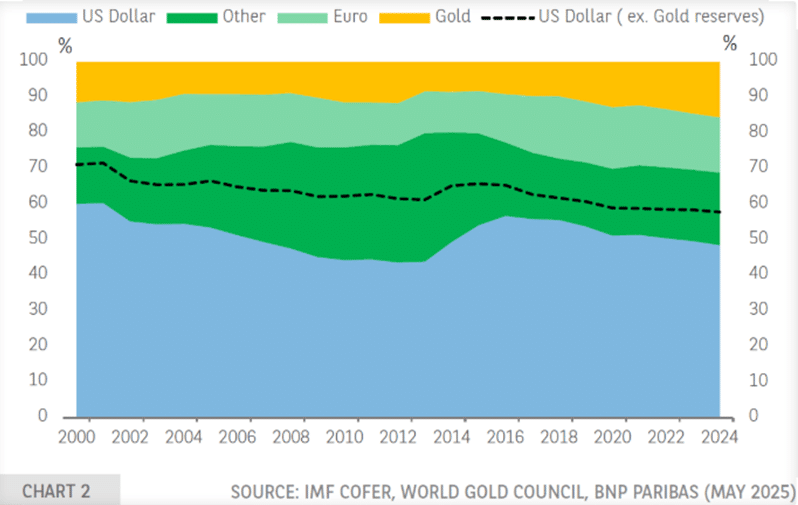

Second, the extent of US economic and financial dominance has declined meaningfully in relative terms. While there is still no single credible alternative that could aspire to replace it, there are now a number of options for diversification that did not exist then, most notably the euro.

Third, policy credibility: whereas in 1971, like now, the macroeconomic imbalances affecting the US were primarily of its own making, in 1971 there were no concerns about public debt sustainability (debt to GDP ratio was 35%), policy unpredictability or unreliability of trade deals signed.

Fourth, dependence: while in the 1970s, the US was still a net creditor to the rest of the world, its Net International Investment Position (NIIP) is now negative by about 90% of GDP, more than double its level of even just 10 years ago. Foreigners hold nearly 20% of US equities and 30% of its public debt (respectively an all-time high and 3x the 1971 share).

Lastly, optionality: most countries now have floating exchange rates, so do not actually need to hold large amounts of reserves, or at least not as large as they do. Indeed, this explains why some diversification away from the dollar has already been taking place since the turn of the 21st century, albeit at a gradual pace. The euro’s share meanwhile has been steady at around 20%.

International Reserves System

Where to from here?

Isabelle Mateos y Lago explains that it is important to distinguish between the role of the dollar in the international monetary and financial system and the dollar exchange rate. In both cases, foreigners have agency, but the outcome will be overwhelmingly determined by choices made by US policymakers.

“The role of the dollar in the system will depend on whether the safe haven properties of the currency are protected or undermined further,” adds Isabelle Mateos y Lago.

The level of the dollar, on the other hand, will be determined primarily by global investors’ appetite for holding US assets, and US investors’ appetite for owing assets from the rest of the world, which in turn will be driven by their respective assessments of the risk-adjusted returns they can expect for both types of assets.

For now, the world has turned less optimistic about the US medium-term growth prospects and less pessimistic about those of Europe. But the US economy retains formidable advantages over its would-be competitors, notably its scale, capacity to innovate and leadership in all advanced technologies that are essential to raise productivity.

Isabelle Mateos y Lago concludes that rumours of the dollar’s demise appear to have been greatly exaggerated, although recent US policies have opened space for its dominance to recede: how that space is filled is up to the rest of the world.

(1) The 10 largest FX reserves holders are, in decreasing order of size of reserves: China, Japan, Switzerland, India, Russia, Taiwan, Saudi Arabia, Hong Kong, SAR, South Korea, and Mexico.

Read the full report

Visit the Economic Research – BNP Paribas portal for more information