Key takeaways

- Europe’s green, digital, industrial and defence ambitions require annual funding flows well above historical levels.

- European banks’ profitability has improved since 2022, but structural gaps with US peers remain.

- Banking Union, capital markets integration and a balanced prudential framework are central to strengthening Europe’s financial sovereignty.

In a recent publication, BNP Paribas’ Economic Research department explores the role of banking competitiveness in European sovereignty. As the energy transition, reindustrialisation, digital transformation, innovation and defence will all require significant financing flows in the coming years, the European Commission’s recent consultation on the banking sector’s competitiveness points to the need for a banking system that can finance these ambitions. Completing the Banking Union, advancing capital market integration, and ensuring a balanced prudential framework will be key.

Why does banking competitiveness matter for European sovereignty?

According to BNP Paribas’ Economic Research department, with banks providing nearly three-quarters of all financing in the EU, their ability to lend and compete internationally is central to Europe’s ability to fund its strategic ambitions.

The author observes that without strong European banks able to increase their financing capacity, Europe would rely more heavily on non-European financial institutions, which already expanded their foothold across various investment‑banking segments.

While significant progress has already been made in banks’ ability to address the rise in funding needs, advancement is needed in adapting prudential requirements to new challenges and increasing capital markets integration, as highlighted in the Letta and Draghi reports.

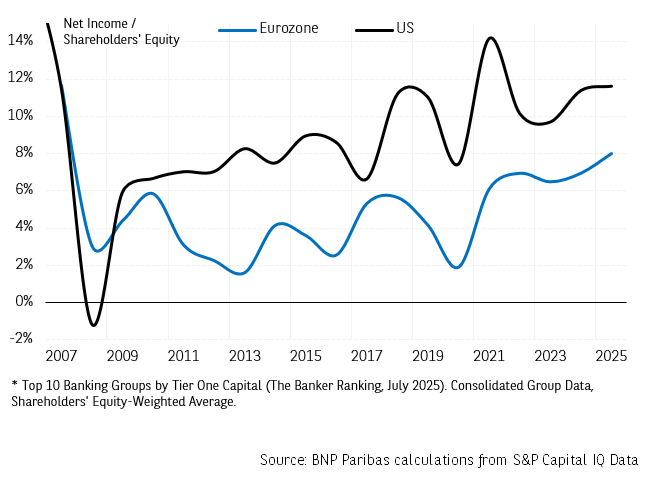

European profitability stronger, but gap with US banks remains

BNP Paribas Economic Research notes that the normalisation of rates since 2022 has contributed to the profitability of major European banks, although disparity with US banks remains due to their greater reliance on markets, meaning higher commission income and lower capital consumption. This gives US banks greater capacity to finance growth and invest in new businesses.

Chart 1: Comparative Profitability of Major European Banks and US Banks

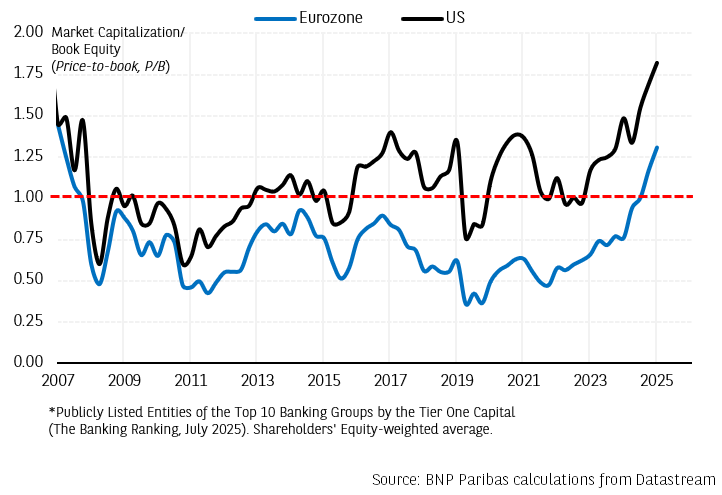

The author also points out that European banks’ average price-to-book ratio exceeded 1 in 2025 for the first time since 2010, suggesting that expected returns now cover investors’ cost of capital. Yet US banks continue to benefit from stronger valuations.

Chart 2: Comparative Equity Valuations of Major European and US Banks

Prudential framework must remain balanced

The author highlights the EU’s strengthened banking framework since the global financial crisis, with Basel III transposition, the reduction of variability between internal models and the final Basel III package adoption, particularly the output floor from 2025. However, the author notes that while European banks are among the best capitalised and most closely supervised, he points to the importance of calibration in light of the BIS’s work suggesting that beyond the current level of CET1 ratios, gains in financial stability from a further increase in capital requirements are modest, while the costs in terms of financing capacity remain considerable.

❝ Striking the right balance is now crucial to maintain the soundness of the European banking system without hampering potential growth. ❞

Reducing fragmentation to unlock financing capacity

European banking competitiveness is constrained by the unfinished Banking Union according to the author, especially the absence of a common European liquidity framework for resolution. He notes that such fragmentation limits economies of scale, raises funding costs, restricts flows and hinders cross-border consolidation, creating uneven financing conditions across countries.

Greater capital markets integration would improve risk-sharing and strengthen financial stability, according to the author. Additionally, the revival of securitisation could support by freeing up bank capital for new lending, while a clearer and more predictable regulatory framework would reduce uncertainty.

Strengthening European banks in investment banking

BNP Paribas Economic Research notes that the region’s economy will increasingly depend on banking intermediation, but that more integrated capital markets would improve allocation of savings in the EU and drive availability of finance.

By postponing, in early June 2026, the implementation of the FRTB to 1 January 2030, the European Commission aims not to introduce a competitive disadvantage, as this overhaul of capital requirements relating to the trading book is not yet enforced by either the United States or the United Kingdom.

For more information, please visit: Economic Research – BNP Paribas