The

fight to tackle climate change is gruelling, multidimensional, and set to last.

In order to succeed, several factors need to be considered. Within this complex

ecosystem, transport – both individual and public – plays an important role. It

is at the heart of our daily existence: railways, for example, have been the

foundation of entire nations.

In

that context, the progressive evolution of the transport sector towards a

greener, more sustainable model is significant – and is having an impact on

both society as a whole and us as individuals.

At the same time the transport sector is essential both from a social and economic standpoint. Lowering the carbon footprint whilst developing a more efficient transport system is therefore crucial.

Source: BNP Paribas Green Bond Framework

Personal and mass transport is at the core of our daily life

Transport globally accounts for c. 60% of global oil consumption and almost a quarter of the world’s CO2 emissions [Source: World Bank, 2015]. It therefore represents a significant contribution to climate change.Efforts are being made across the sector, from fuel-efficient aeroplanes to optimised logistic networks and lower-consumption ships. For most people, however, daily experiences are shaped significantly by cars and mass transit systems, especially trains. As a result, these segments of the transport sector tend to receive more attention.

Petrol and other fuel used in engines account for the largest portion of fossil energy consumed in the transport sector.

Motor gasoline remains the largest transportation fuel, but its share of total transportation energy consumption declines from 39% in 2012 to 33% in 2040. From 2012 to 2040 the total transportation market share of diesel fuel (including biodiesel), which is the second-largest transportation fuel, declines from 36% to 33% and the jet fuel share increases from 12% to 14% in 2040.

Source: U.S. EIA, 2016

Early

efforts to develop “green” fuels based on ethanol and other by-products of

agriculture to replace carbon fuels in traditional engines are now being phased

out. The technology behind electric powertrain systems has reached a degree of

maturity that, in combination with decreasing battery costs, paves the way for

mass commercial deployment. Trains and urban transport systems were the first

to evolve in that direction but the hype curve has been directed toward cars.

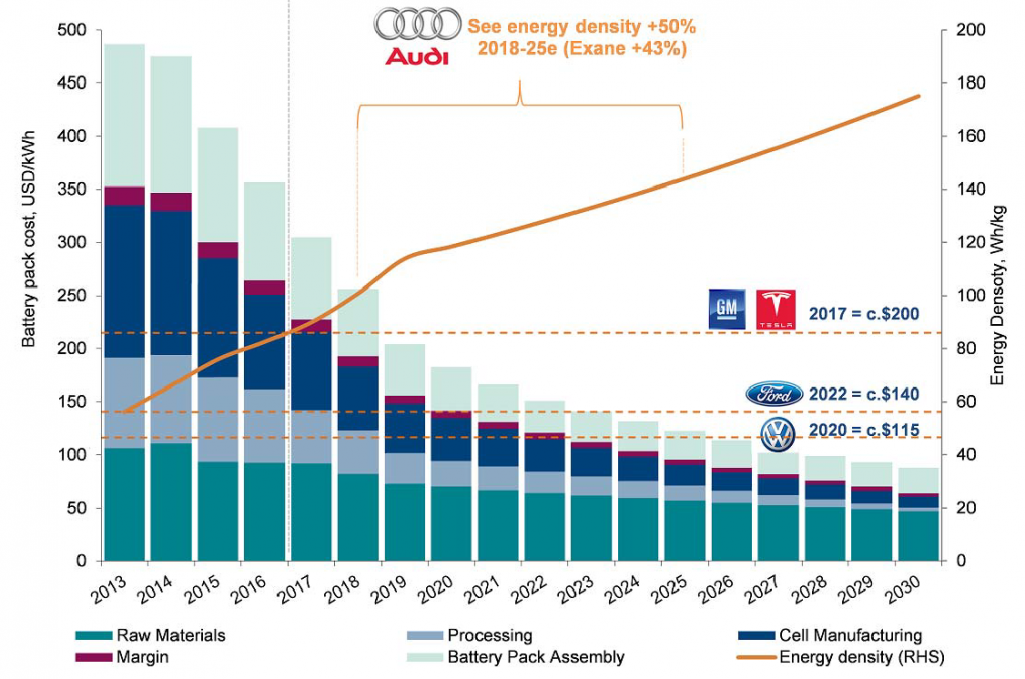

Industry battery pack costs now look to be heading to c.USD120/kWh by 2025e.

Source: Exane BNP Paribas, 2017

But the increasingly prevalent use of lithium-ion batteries and the hype surrounding electric vehicles have brought the electric car back to the centre of the conversation, helping to create the high-end, value-driven, demand from consumers necessary to jumpstart real long-term change.

In that regard, the rise of Tesla gave a nudge to the entire market that was driven by the slow long-term investments in research and in infrastructures to accelerate the momentum of the electric vehicle market.

Electric cars are also catalysts for more general behavioural change. With electric cars on the march, some of the possible drawbacks of sustainable electricity generation need to be better understood. The spread of battery-based electric cars could also bring an unexpected ancillary benefit to the entire world’s energy transition by helping with the deployment of massive mobile energy storage capacities offered by hydrogen connected to the grid on an interim basis.

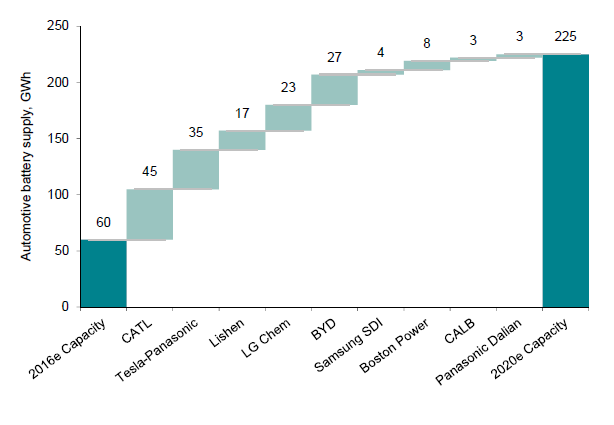

Battery supply is being expanded aggressively

but much, much more will be required post 2020

Smart and sustainable mobility is at the core of largest companies’ strategies

But now, even the sector’s flagship affiliated sport is experimenting with new kinds of engines. The launch of the Formula E in 2011 mirrored the meteoric rise of Tesla overtaking the historic “Big 3” of the American traditional industrial states. A success that followed the announcement of the Tesla Model 3 was almost too overwhelming for the company that has been struggling to match the demand with production. In the background, the Renault-Nissan alliance, the “Big Four of China’s automotive market” (Shanghai GM, Dongfeng, FAW and Chang’an), GM, Volkswagen Group and BMW have made strong inroads in what remains, despite the headlines, largely only a niche – albeit of high value-add – of the market.

Behind the attention-grabbing headlines and the hype, most producers globally have also made smart mobility a key part of their long-term strategic pivot. Most manufacturers in all regions are – more or less slowly – following the trend and are launching a line-up of electric and hybrid cars. As investment in electric vehicles has grown, autonomous cars appeared on the horizon, potentially revolutionising the industry at an even faster pace.

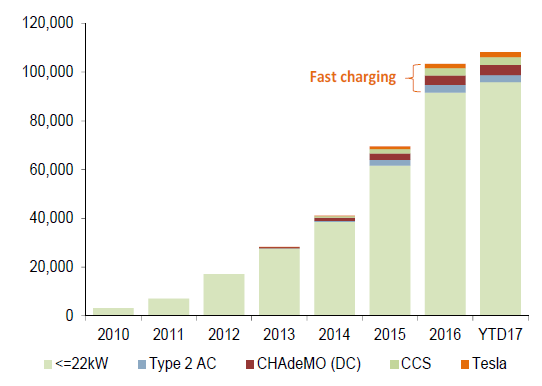

Despite a relatively slow start, sales of electric vehicles have already hit the one-million mark in Europe. The market is therefore preparing for fast adoption, supported by the investment made from both the public and private sector. This investment is crucial for the development of the charging infrastructure required to support the expansion of the electric vehicle market. In Germany, some auto-manufacturers have committed to deploy several thousand fast charging stations by 2020. This commitment shows a determination to remove hurdles for the mass roll-out of electric vehicles.

Government incentives and investment – notably

in China – is accelerating the growth of electric charging networks

Regulation

and political support are key enablers of the market (e.g. California’s set

targets by 2025, [Source: IRENA, 2017]), and early success in countries like

Norway and Netherlands, where electric car penetration is already high, is

helping to set the stage for a broader roll-out. Given the current momentum,

the market may soon be reaching critical scale and therefore potentially having

a materially positive impact on the environment. This is if some of the

technical and behavioural shortcomings, which limit adoption today, are

addressed in the coming years.

Measuring the interference on the electric market

Despite the hype (and potentially huge impact) surrounding electric vehicles in the automotive industry, we also need to be mindful that this revolution is likely at least a decade away.Electric cars are not a speculation about an unproven – albeit coming – technology with a much longer adoption and investment cycle; they increasingly are the reality of the auto industry.

However, for their advantages, they still face headwinds on the road to mass adoption.

As always, the most significant challenge is economic. The total cost of ownership (TCO) of an electric vehicle is still high, despite various policies and tax incentives having been put in place. The cost per kWh is decreasing with production volume, but still lags that of a combustion engine. For smaller cars (e.g. A/B/C segments), it is expected that the cost-equivalent point for car makers will be reached in three-to-five years, i.e. the point at which the profit generated from an electric car is equal or higher than that of a traditional combustion engine car, and is hence seen as a critical point for mass adoption.

Furthermore, electric powertrains face an energy density problem that makes cars today lag their combustion peers in terms of range. While this may not be relevant for all cars (for e.g. smaller cars which are actually not driven a lot), range and infrastructure remain a hurdle for drivers’ willingness to adopt, particularly given the emotional resistance to switch in case the need for a longer-distance trip would ever arise (e.g. an annual holiday).

Finally, issues like charging time (increasingly being addressed with the recent generation of chargers and a transition to larger batteries), breadth of the required charging infrastructure to allow for common use, and production capacity allowing production of both the cars themselves and the vital battery components (especially the lithium used in lithium-ion batteries), are still being addressed. The constant production delays faced by Tesla for its Model 3 (cf. Bloomberg Model 3 tracker) highlight the market’s long awaited hockey stick growth is still in its infancy.

A Hybrid view of the Near Future

While the electric vehicle industry matures in its market reach and industrial capacity, the most significant evolution of the automotive market over recent years has been the success of hybrid vehicles, combining both electric and combustion engine powertrains. These cars are not as ecological as full electric vehicles, but have already provided strong progress in their ability to reduce fuel consumption and optimise the energy yield of a car.In addition, they offer performance comparable to that of a combustion car, especially in terms of range, and benefit from not depending on battery charge time. Most, if not all, manufacturers have brought a range of hybrid vehicles to the market, as a spearhead to address increasing customer demand.

But here too, despite the strong performance of hybrid cars and high press coverage, the market reach has stalled at a relatively modest level, representing below [5%] of new cars being sold in the US. Two markets – USA and Japan – account for the largest portion of the global market by far. A major reason for this is price; despite advantages on TCO, the purchase price for hybrid vehicles is relatively high. Hybrid vehicles by definition are home to two powertrains, the cost of which car makers struggle to pass on to customers.

However, with consumers increasingly adopting a more sustainable mindset, and the expanding breadth of hybrid models on offer in the coming years, the segment could experience strong tailwinds in the coming decade.

Regulations as a catalyst

The transport sector plays an important role in efforts to contain global warming. If the UN’s goal to limit the temperature increase to 2°C should be achieved, a switch to electric vehicles must become a key objective.While regulation and policies play an important role, the future of electric cars at this stage follows a two-step approach, based on: (1) a subsidised TCO for an interim period, with infrastructure being established and mindset slowly adapting to the new context; and (2), in the medium term, a full transition that features a competitive TCO as well as an efficient industrial ecosystem for electric vehicle production and operation. Another element that needs to be kept in mind when discussing or assessing the environmental impact of electric vehicles is the production mode of the electricity consumed by the vehicle. Too often still a large portion of the electricity produced stems from non-renewable sources (fuel or carbon) or from nuclear sources, and the expected increase in consumption will require further electric production which could end-up being serviced by fossil-based energy plants. Hence as long as the input side does not mirror a transition to sustainability, it will hardly be possible to achieve the desired environmental impact.

In parallel to this iconic revolution in the making, societal and technological innovation is also likely to transform the underlying market in ways that are still to be fully laid out. Shared mobility is one of these powerful trends that will play a role, with individuals sharing their cars or accessing on-demand shared fleets.