Growth is local whereas sovereign bond yields are global

Government bond yields in advanced economies have been highly correlated over the past four decades, with moves in US Treasury yields often coming together with significant changes in foreign long-term interest rates, except for Japan.

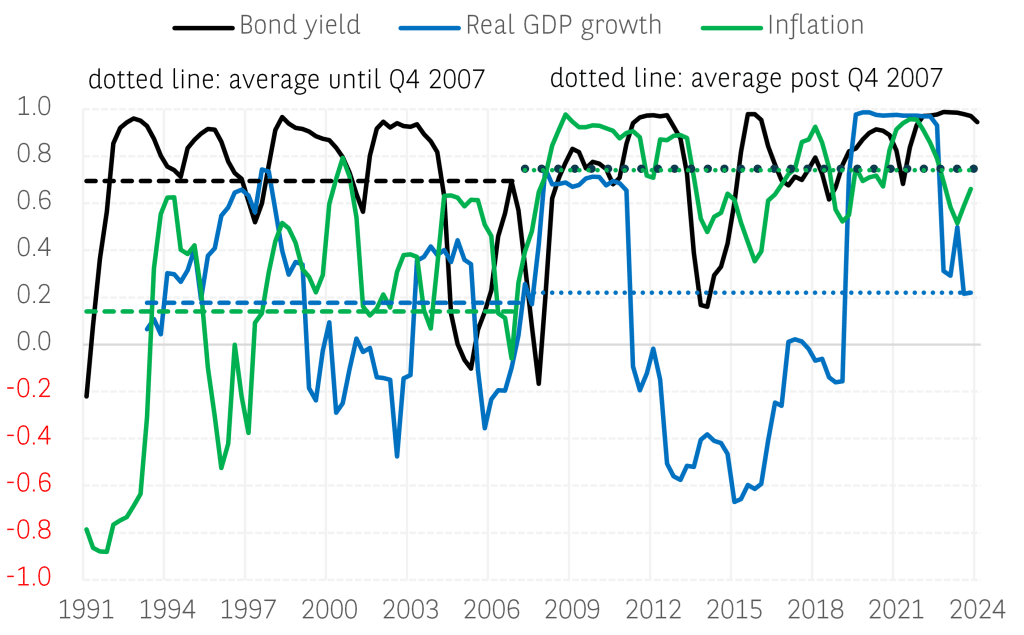

Nominal bond yields are affected by a rather broad range of factors, but growth and price dynamics play a particularly important role, directly or indirectly. In this context, the co-movement of bond yields raises the question of whether real GDP growth and inflation are also highly correlated.

William de Vijlder, economic advisor of the general management, in a recent publication, observes that the global co-movement of bond yields is higher than that of real growth or inflation, providing insights on these dynamics and explaining why it matters to various actors of the financial ecosystem:

❝ Considering that the correlation between the US and the euro area in terms of real growth is well below that of government bond yields, it is tempting to conclude that growth is ‘local’ whereas sovereign yields are determined in a global market. ❞

With the correlation between the US and the euro area in terms of real growth well below that of government bond yields, William de Vijlder concludes that growth is predominantly driven by domestic demand whereas sovereign yields are to a large extent determined by global factors. True, the reality can somehow be more complex as foreign growth stocks create spillover effects, in particular in the most export-oriented economies.

Similarly, domestic bond yields can be impacted by local monetary policies and local public sector borrowing requirements. This was recently evidenced by the jump in Bund yields as opposed to relatively subdued change in US bond yields, as markets accounted for the prospect of high government borrowing in Germany, to strengthen the country’s infrastructure and defence, in March this year.

The bilateral correlation of government bond yields is higher than that of real growth or inflation

Rolling correlation between the US and Germany (quarterly data, 12 quarter window)

Sources: BNP Paribas, LSEG

Why does it matter that growth is “local” and bond yields “global”?

William de Vijlder has identified four key reasons why it matters with implications for various actors of the financial ecosystem.

First, while higher real yields can indicate an improving growth outlook, they could also be driven by foreign factors and as a result slow down economic growth.

Second, this co-movement of sovereign bond yields has important implications for central banks, as it impacts the transmission of monetary policy to the real economy.

Third, it influences the gap between the cost of borrowing and the cashflows that serve to reimburse the debt. As such, governments should keep in mind that a lack of fiscal discipline can create negative externalities by pushing up bond yields abroad. This is particularly important for the US, given its central role in the global financial system, but also for EU fiscal governance.

Last but not least, it matters because of the very large financing needs required to strengthen and develop infrastructure and public goods such as education, healthcare, and defence, to finance the energy transition and digital revolution. Against this background, every issuer of debt should prepare for the possibility of higher interest rates and stress the resilience of its balance sheet.

Read the full report

Visit the Economic Research – BNP Paribas portal for more information