On 1 January

2020, the shipping industry will enter new waters as the rules from the

International Maritime Organization (IMO) to reduce sulphur oxide emissions

come into effect. The more stringent regulation is in response to heightening

environmental concerns, contributed in part by harmful emissions from ships.

Why does this matter? And what will it mean in practice?

Victoria Harbour, Hong Kong

Shipping companies whose vessels still consume the current low grade 3.5% sulphur content bunker fuel now have just a few months to meet the new IMO standards. So how will industry players navigate a changing shipping industry?

Solutions for sustainable shipping

Alternative energy options – wind power and other renewables – are either years away or impractical, so most vessels will continue to use fossil fuels for the foreseeable future.To meet the regulations, firms can choose to:

- Switch to low-sulphur (LS) bunker fuel by modifying the vessel’s engine to ensure it can run on LS fuel or by mixing an additive to ensure the LS’s viscosity is the same as the old high-sulphur (HS) version,

- Continue with HS bunker fuel and fit a scrubber – which cleans the exhaust gas – to remove sulphur and other fine particles, or

- Adopt Liquefied Natural Gas (LNG) or methanol-fuelled engines, although these technologies are still at an early stage of deployment.

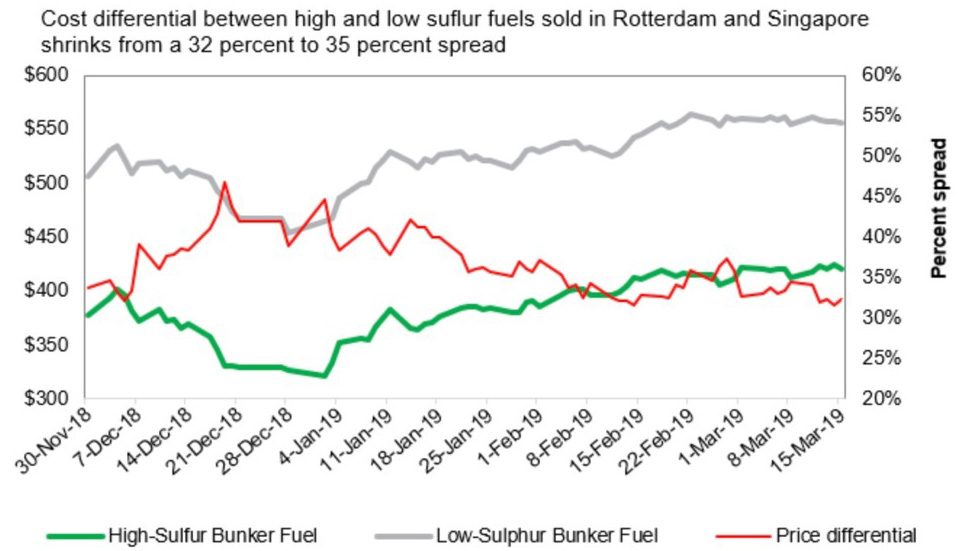

Despite these alternative options, three challenges further complicate these calculations. The first is cost; LS bunker fuel is currently one-third more expensive than HS fuel – by about $150/ton (see chart).

Price spread between high and low sulfur fuels narrows

Scrubbers are not cheap either: at a cost in the range of $2.5m to $5m per vessel, they are easier to justify on a very large crude-carrier than on a small dry-bulk vessel. The payback is typically three to five years, depending on the type of vessel and the spread between the cost of LS and HS bunker fuel.

A second challenge to using cleaner fuel is that supplies are uncertain. It is up to refiners to provide the less-polluting fuel, and some shippers fear shortfalls, at least in the short term. [2]

And thirdly, many ships are not operated by their owners, but are leased to third parties that run them for defined periods, e.g. on five-year contracts. In that case, who should pay? The lessee, who funds the operating costs, including the bunker fuel, or the lessor, who owns the ship?

Green finance

Meeting the requirements of IMO 2020 may lead to additional expenses – and green financing can play a key role. According to Nicolas Parrot, Head of Transportation Sector, Investment Banking Asia Pacific at BNP Paribas, the recent growth of green financing means there is now a range of ground-breaking solutions to support shipping firms that wish to reduce their environmental footprint. “The main options today available include green loans and bonds, and sustainability-linked loans (SLLs [3]),” he says. “Within this mix, the range of expenditures that qualify for green financing has grown significantly in recent years.”

There are, of course, differences between the options. Funds raised from green loans and green bonds must be allocated to eligible green capital expenditure such as scrubbers or LNG engine retrofit, which are classed as providing environmental benefits. That classification allowed one of Singapore’s leading fleet owners to fit scrubbers on its vessels in November 2018 with the financing coming from a green loan arranged by BNP Paribas – a first in the Asia Pacific region.

Aside from steps to meet the IMO 2020 requirements, green financing is also available for other sustainability improvements, such as using a more fuel-efficient propeller, fitting a ballast water-treatment system, refitting to run on methanol, and supporting research and development costs.

Yet, even as the industry reduces its environmental impact, challenges remain – not least in the Asia Pacific region, where many smaller firms do not have sufficiently large green capex projects to allow it to access the green debt market. Here, sustainability-linked loans, or SLLs, could play a vital role.

Sustainability-linked loans

Source: Bloomberg New Energy Finance, as of June 3rd 2019

What makes SLLs different from other green financing options is that they provide a generic source of funding for corporate purposes without any specific use of proceeds. They are based on specific sustainability performance targets (“SPT”), including industry- and company-relevant key performance indicators (KPIs), external Environmental, Social and Governance (ESG) ratings – or a combination of both. SLLs can therefore assist smaller shipping firms that wish to move towards a more sustainable operating model.

The sustainability element is addressed in one of two ways:

- The borrower’s ESG performance as independently assessed by an external agency on an annual basis.

- KPIs that reflect the sustainability goals of the borrower –

for example, around the carbon-intensity of their business. This approach may

be better suited to smaller shipping companies that may not have external

ratings.

“The IMO 2020 sulphur-emissions limits are not the first environmental regulation that the world’s most important transport sector will have to meet, and they won’t be the last,” reckons Parrot. “For instance, companies will soon need to comply with the Ballast Water Management Convention and the IMO 2050 CO2 targets. As the industry continues to reduce its environmental impact, it will need greater access to new, efficient sources of finance as shipping firms chart their course in a greener world.”

[1] Air Pollution and Energy Efficiency, IMO (August 19, 2016).

[2] Low-sulphur fuel supply fears wane; price still unclear, JOC.com (March 21, 2019).

[3] These were previously known as Positive Incentive Loans (PILs).