What sparked investors’ growing interest in stablecoins, and how did it become a multibillion-dollar market? It all began in the mid-2010s, with Tether and Circle, the two leading US dollar-linked stablecoins issuers, playing a pivotal role in shaping the market for this asset class. In 2014, Tether launched USDT followed by Circle’s USDC in 2018 which was positioned as a potential low volatility alternative to traditional cryptocurrencies. While decentralised finance (DeFi) is probably the main use case for stablecoins today, in a recent report, BNP Paribas Equity Research assessed their potential to disrupt the payment ecosystem.

Projected to exceed USD8 trillion in transaction volume this year

Stablecoins are digital assets whose value is designed to track the value of an underlying asset or another unit of value, such as fiat currencies like the US dollar and the euro. Exchangeable on blockchain like other cryptocurrencies such as Bitcoins, stablecoins are tradable on crypto exchanges such as Coinbase or Binance.

❝ As regulation frameworks, focused specifically on stablecoins (notably in the US and the EU) are being implemented and mainstream payment players like PayPal and Stripe are embracing stablecoins, we expect trust to become less of an issue, both on the consumer and on the merchant sides. ❞

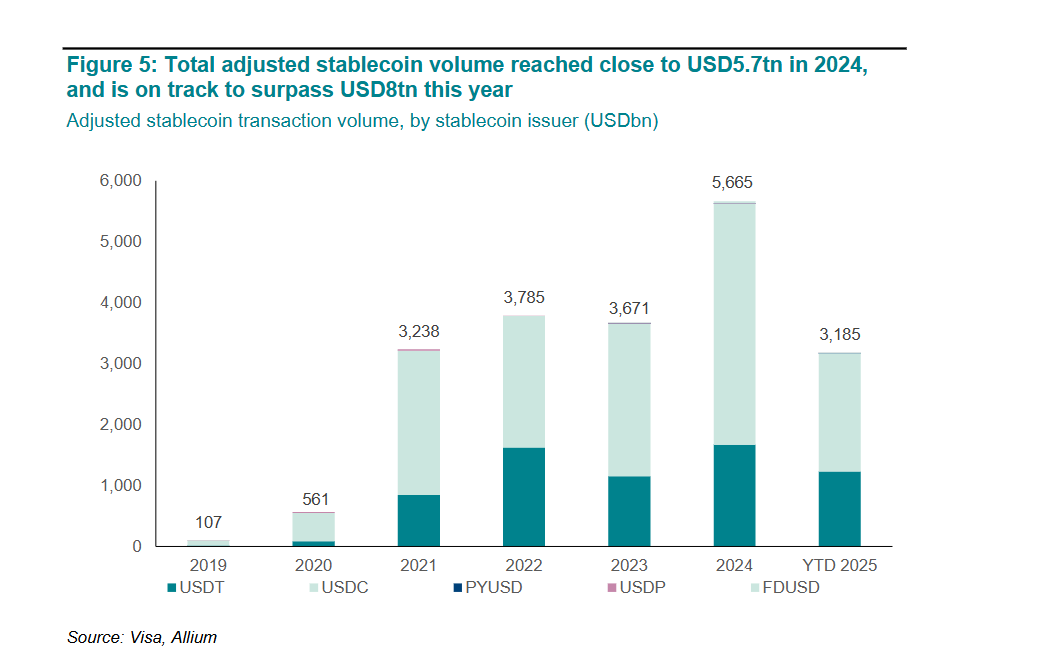

USDT and USDC currently dominate the global scene with more than USD150 billion and over USD60 billion in circulation respectively. According to Allium, a blockchain data platform, adjusted stablecoin transaction volume reached close to USD5.7 trillion last year. With volumes approaching USD3.2 trillion in June this year, the blockchain data platform estimates they can reach as much as USD8 trillion in 2025.

Such momentum stems from rapid technological refinement and regulatory clarity, particularly across the United States and the European Union. Observing this surge, our analysts note that although historical issues like volatility, scalability and costs are gradually being addressed, the debit cards’ value proposition seems strong enough to deter the competition. While cross-border use cases look more promising, there are also already several fintech players that have successfully disrupted this market.

❝ And yet, stablecoin-based payment still doesn’t bring much incremental value in our view, outside of cross-border use cases currently. ❞

Regulatory clarity supports growing investor interest

Investor interest for stablecoins has grown significantly lately, as evidenced by Circle’s June 2025 IPO, Stripe’s USD1.1 billion acquisition of Bridge, and PayPal’s efforts in 2023 with its own stablecoins. Regulatory clarity has played a large role, as explained by BNP Paribas Equity Research analysts.

U.S. Genius Act

In the US, the “Guiding and Establishing National Innovation for US Stablecoins of 2025”, or GENIUS Act, was approved by the House of Representatives on 17 July 2025, and signed by the US President on 18 July. It sets a new framework for regulating stablecoins and their issuers by prioritising consumer protection, operational standards and anti-money laundering compliance: in short, strengthening transparency and trust in this digital asset space.

MiCA in the European Union

In the EU, the European regulation on Markets in Crypto-Assets (MiCA) provisions for stablecoins came into application in late June 2024. From then on, stablecoin issuers must obtain approval from relevant member state authorities before offering their tokens within the EU, or when offering stablecoins pegged to the euro or other member state currency. This means that algorithmic stablecoins are banned.

Regulatory clarity in the US and the EU is an essential step towards scaling up the stablecoin ecosystem. Next, regulation will also have to evolve in emerging markets, destination countries for remittances, and where local fiat currencies are volatile for stablecoins use cases to really take off.

Assessing the disruptive potential of stablecoins in payments

BNP Paribas Equity Research is discerning that stablecoins do not currently have the potential to disrupt most payment use cases. While blockchain-based transactions can bring speed, cost and access benefits, our analysts observe that debit cards already perform admirably on all these three fronts.

Moreover, the user experience can be cumbersome for many. In a direct crypto-wallet-to crypto-wallet P2P transaction, it is often hard for non-crypto experts to understand the mechanics of the transaction and associated costs. Typically, the sender needs to paste a long wallet address to identify the recipient of the stablecoins, choose the blockchain used for the transaction, which must be compatible with the receiver’s crypto wallet, while network fees may be displayed in the native crypto of the blockchain used. Additionally, stablecoins still incur relatively significant on-ramp and off-ramp costs, and the lack of consistent regulation across jurisdictions creates uncertainty for issuers and users alike.

Personal or B2B cross-border payment use cases look more promising, given that stablecoins can transfer in near real time between crypto wallets across the globe at minimal cost. Yet, our analysts found that stablecoin-powered solutions would still struggle to compete against various fintech players that started to disrupt the industry decades ago.

For more details on BNP Paribas Equity Research, please visit:

Cash Equities | Global Markets

BNP Paribas does not consider this content to be “Research” as defined under the MiFID II unbundling rules. If you are subject to inducement and unbundling rules, you should consider making your own assessment as to the characterisation of this content. Legal notice for marketing documents, referencing to whom this communication is directed.