Global responsible investments have been growing steadily across developed countries. Between 2012 and 2014, sustainable investment rose from USD 13.3 trillion to USD 21 trillion, with the US being the fastest-growing region during this period, followed by Europe and Canada. This 61% growth outpaced the growth of total professionally-managed assets over the same period.

Sustainable investing, SRI, responsible investing, ESG investing… What’s it all about?

Broadly speaking, responsible investing is an investment approach that factors Environmental, Social and Governance (ESG) criteria into investment strategies and policies. However, ESG approaches encompass a wide range of strategies, from negative/exclusionary screening (removing companies or sectors), best-in-class screening (selecting best performers within a sector using ESG criteria), norm-based screening (assessing companies against specific standards or norms), ESG integration (inclusion by asset managers of ESG factors into financial analysis and investment decisions), sustainability-themed investing (targeting certain themes around sustainability), impact investing (to generate both a financial return alongside a social one) and companies’ engagement and shareholder vote.Between 2012 and 2014 exclusionary screening was the largest strategy (USD 14.4 trillion), followed closely by ESG integration (USD 12.9 trillion) and corporate engagement/shareholder action (USD 7 trillion).

What is driving growth in responsible investment?

Reputation

In this context, the voluntary adoption of codes and standards by investors has been a driving force in shaping the responsible investment market.

The two most widely used standards are the United Nations Global Compact Principles (UN GCP) and the United Nations Principles for Responsible Investments (UN PRI), consisting of six principles that guide investors on factoring ESG considerations into their investment decisions and promoting their use more broadly in the industry.

As of 2015, approximately 1,500 investment institutions have endorsed the UN PRI representing USD 60 trillion.

Regulatory developments

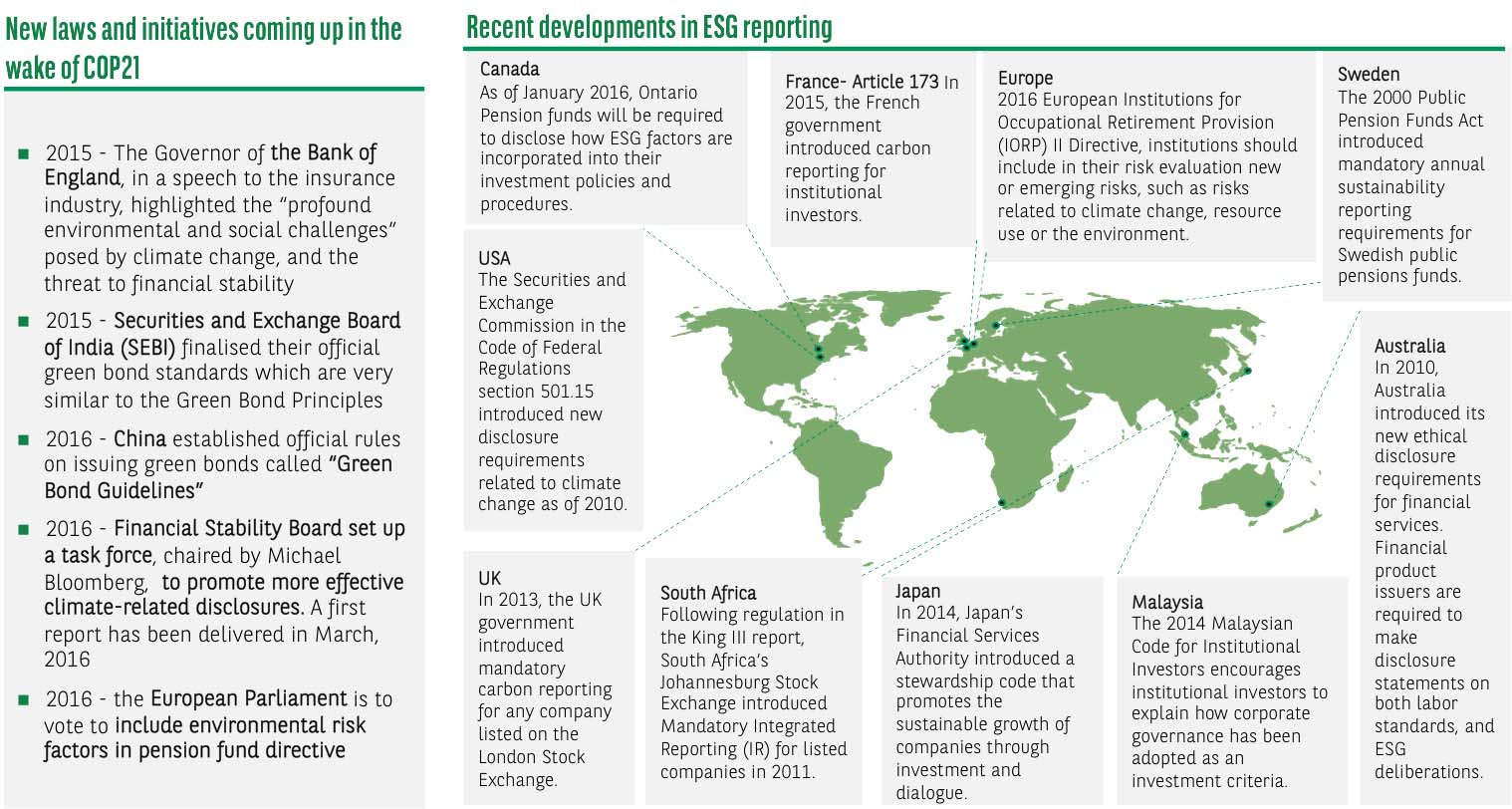

Alongside the development of international codes and standards, countries have started adapting their own regulatory framework and have gradually required institutional investors to take into account specific environmental or social risks when reporting, as well as managing their assets. Some countries started explicitly banning certain areas of investment, such as cluster munitions, as the case of Belgium in 2007, France in 2010 and the Netherlands in 2013.

Some countries have also reviewed the legal framework applying to their pension funds. South Africa for instance amended its Pension Funds Act in 2011 requiring the inclusion of extra-financial analysis in the investment process. Canada took a similar step in 2014 by amending the Ontario Pension Benefits Act to ensure ESG factors are included in investments policies.

Most recently, as climate change has been put at the forefront of the international community agenda, increasing regulatory pressure for carbon-related disclosure has fuelled demand for sustainable investments. In the wake of the recent historical agreement in Paris where 195 states committed to capping temperature increase to 2?C, regulatory developments are expected to materialise in the near future as they will need to live up to their commitments.

France is already taking one of the most proactive approaches. Article 173 of the French law on “Energy transition for green growth” requires that institutional investors disclose in their annual reports how ESG and climate change considerations are incorporated into their investment policies and risk management. Investors must report on a “comply or explain” basis – in other words, investors will have to provide an explanation if they do not comply with the above requirement. The first report should cover the period from January to December 2016. Welcomed by the European Sustainable Investment Forum (Eurosif) as a “ground breaking measure for the investment community”, the law is actually closing the loop from a 2010 French Law (Grenelle II) that required specific ESG reporting for asset managers (article 224).

Market-driven initiatives bring climate-risk investment into the mainstream

Long-term institutional investors are increasingly concerned by new financial risks linked to the transition to a low carbon economy, such as stranded assets for fossil fuel and, more particularly, the coal sector. In this regard, the Norges Bank Investment Management mentions that “the expected increase of regulatory measures and the unfolding physical impacts of climate change are likely to represent a major economic transition, with losses and gains distributed to market players depending on their strategies in this process”.

In response to these risks a large number of investors have started taking a proactive approach to reduce carbon exposure of their portfolios through initiatives such as the Montreal Carbon Pledge and the Portfolio Decarbonisation Coalition. By signing the Montreal Carbon Pledge, investors commit to measure and publicly disclose the carbon footprint of their investment portfolios on an annual basis. The Pledge was launched on 25 September 2014 and has attracted commitment from over 120 investors with over USD 10 trillion in assets under management, as of December 2015. Support has come from investors across Europe, the US, Canada, Australia, Japan, Singapore and South Africa.

The Montreal Carbon Pledge allows investors (asset owners and investment managers) to formalise their commitment to the goals of the Portfolio Decarbonisation Coalition, which mobilises investors to measure, disclose and reduce their portfolio carbon footprints. Over USD 100 billion has been committed to this as of December 2015.

Last November, Sweden’s national AP Pension funds have also agreed to coordinate the way they report the carbon footprints of their investment portfolios.

In December 2015, the Financial Stability Board set up a task force on climate-related financial disclosure, chaired by Michael Blomberg. The objective of the task force will be to help improve carbon-related disclosure by corporate to better inform investors’ decisions.

With increasing investor awareness of carbon asset risks and following the momentum generated by the Paris Agreement, 2016 has seen a climate-related shareholder decisions come to the fore. For instance, the Aiming for A coalition of UK asset owners, representing GBP 230 billion assets under management, is advocating and filing resolutions for improved management and disclosure of climate risks and opportunities within the companies they own. Aiming 4 A has secured successful shareholder resolutions at prominent energy firms and is calling for the major mining companies to increase disclosure on their climate change strategy.

A broader interpretation of fiduciary duty

Fiduciary duty has long been a contentious issue, which investors have cited as a reason for not incorporating ESG into investment decision making processes. Indeed, there were concerns that fiduciary duty, which is about ensuring the best investment returns, could potentially conflict with ESG-based investment. However the debate has recently shifted dramatically. A 2016 report from the UN PRI concluded that failing to consider long-term investment value drivers in investment practice – including environmental, social and governance issues – is a failure of fiduciary duty.

Enhancing risk-return – and performance

Institutional investors are increasingly seeing ESG indicators as material and key to add value over their long term investment. According to a 2015 Mercer study on ESG, approximately 60% of institutional investors believe that incorporating ESG factors in investment decision-making has a positive impact on risk-adjusted returns.More recently, in a 2016 Harvard study on corporate sustainability, researchers concluded that there is a link between sustainability issues and performance as “firms with good performance on material sustainability issues significantly outperform firms with poor performance on these issues”.

In May 2016, 100 investors managing USD 16 trillion of assets and six credit rating agencies, including S&P and Moody’s, signed a statement calling for the integration ESG in credit ratings.

In sum, reputation, regulation and risk mitigation – in particular climate risk – are driving institutional investor appetite to factor ESG into their investment strategy and decision-making process. With the integration of environmental, governance and social criteria, sustainability is gradually becoming mainstream for large asset owners in developed countries. Those leading the way have clearly understood that both financial and ESG factors are key to enhancing their risk-return as well as reconciling short-term and long-term objectives.

Source: BNP Paribas