The MSCI’s move to start the inclusion of

Chinese A shares in their indices from next June has prompted a dramatic

rethink as active fund managers scramble to reexamine China’s sprawling equity

markets. But as offshore funds ponder an uncertain foray into what until now

has remained largely unchartered territory for global investors, there are

plenty of reasons to be optimistic about the New China story.

BNP

Paribas Head of Equity Research, Manishi Raychaudhuri says the New China Index

represents solely the stocks that are benefiting from changing Chinese consumer

preferences.

These stocks will be the disproportionate beneficiaries of A share inclusion, because they represent not only what the Chinese consumers are buying, but also how they’re buying it in the case of the technology-weighted stocks such as Tencent, Alibaba and Baidu. “

Manishi Raychaudhu, BNP Paribas Head of Equity Research

The numbers tell a compelling story in that China’s

economy still has far to go in boosting private consumption to catch the US,

its nearest counterpart, which shares a similar land mass but only one fourth

of its population.

Where the US owns 797 cars per every 1000 people,

China owns 83 [1].

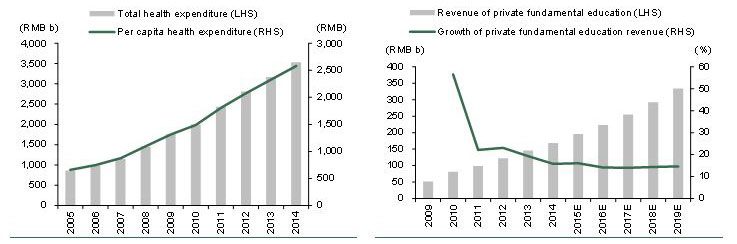

Healthcare spending in the US sits at 17 per cent of total GDP versus 5.5 per

cent in China[2].

China’s insurance penetration is half of the US’s 8 per cent, while public

spending on education sits around US$10,400 per student in the US versus just

US$4,900 in China. China’s internet users per 100 people also lags, at 50.3

compared to 74.5 in the US. [3]

This gap is closing fast, driven by the dominance

of Chinese technology giants like Tencent and Alibaba. But beyond the big names,

institutional investors are still reluctant to take the plunge into China.

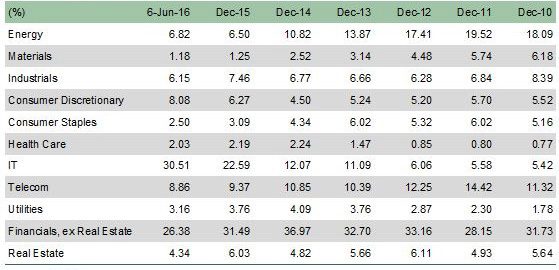

The S&P New China index, which is comprised of

around 29 per cent Chinese A shares drawn from consumer discretionary,

healthcare, insurance, technology and new industrials (outside of the old

manufacturing areas of steel and cement), has outperformed the HSCEI Index by

around 16 per cent over the first half of 2017 [4]. This outperformance is cause

for optimism, despite lingering concerns over Chinese equity markets in the

face of the monster economy’s slowing headline growth.

We’ve seen strong interest recently, particularly since the MSCI announcement, to really understand how to get a foothold in China. What the New China Index does is exclude “old China” sectors where the market continues to harbor long term structural concerns, financials for example, and gives investors a solution to position themselves in only the sectors with robust growth, without having to take specific stock risk.

Natalie Shaw, BNP Paribas Head of Equity Distribution for Asia Pacific

BNP Paribas believes A share inclusion will be a

positive catalyst for Chinese equities, adding USD 3.2 trillion in total market

capitalisation from the 222 included stocks.[5]

“Inclusion should boost investor sentiment and, over the long term, flows into China. It also helps President Xi Jinping’s ambition to make the renminbi a global currency. The New China story remains the strongest field of growth for the economy and therefore represents the most ideal vehicle for positioning at the moment.”

Manishi Raychaudhu, BNP Paribas Head of Equity Research

[1] Source: NationMaster. Data as December 2014

[2] Source: World Bank. Data as December, 2014

[3] Source: World Bank. Data as December, 2015

[4] BNP Paribas research

[5] BNP Paribas Asset Management, UBS Global Research as of 21 June 2017