Key takeaways

- The immediate macroeconomic impact of the 2026 energy shock in Central Europe remains moderate, with restrained inflationary pressure and limited deterioration in confidence indicators.

- European funding is a safety net with the equivalent of 3% of regional GDP from the Recovery and Resilience Facility to be disbursed in 2026.

- External liquidity, current accounts are strong enough to absorb a rise in energy prices, while sovereign financing conditions have not deteriorated markedly.

In a recent publication, BNP Paribas’ Economic Research assesses the resilience of Central European economies to the 2026 energy shock. Having weathered several storms since 2020, they point to four key factors keeping the region relatively resilient in the current environment.

Has Central Europe shown resilience in absorbing the energy shock?

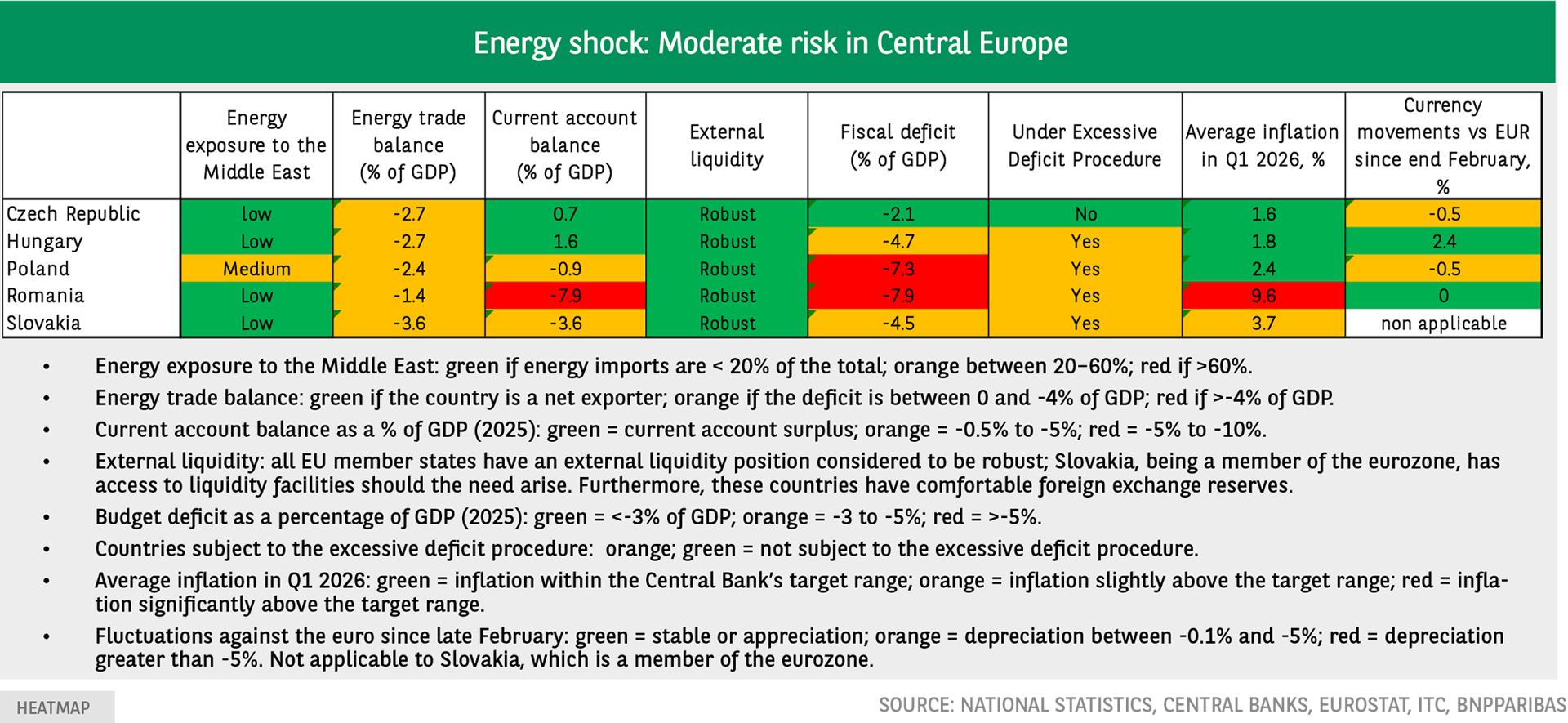

According to BNP Paribas’ Economic Research, Central European economies have so far absorbed the energy shock with limited disruption to growth. Initial March data show that inflation has remained moderate, while confidence indicators have weakened marginally, with manufacturing PMI indices even improving in Poland, the Czech Republic and Romania.

However, the author points to short-term risk factors: all countries in the region are net energy importers, with energy trade deficits ranging from 1.4% of GDP in Romania to 3.6% in Slovakia. Higher logistics and input costs for fertilisers, plastics and aluminium, are expected to feed through into food and durable goods prices. Additionally, the region has many energy‑intensive industries, on top of the automotive sector – accounting for 8.5% of manufacturing value added in Poland and 23.7% in Slovakia – especially sensitive to any pass‑through of higher costs to end prices.

Governments have responded with targeted support measures for households and businesses, including caps on fuel prices and on profit margins of energy companies. Despite limited scope for Poland, Slovakia, Hungary and Romania to provide large‑scale fiscal stimulus due to the EU’s deficit procedure, the author identifies four key drivers safeguarding the region.

Limited supply-side exposure

BNP Paribas’ Economic Research notes that Central Europe’s direct exposure to supply disruptions from the Middle East is currently relatively limited, except for Poland. Meanwhile, strategic oil reserves stood at nearly 90 days of consumption in January 2026, and gas storage levels in March 2026 were around one‑third of capacity.

The author also observes that risks of shortages in key industrial inputs are currently limited: for example, automotive aluminium derivatives and plastics are largely sourced within the EU, while fertilisers used by the agri‑food sector are predominantly supplied from Europe, reducing immediate vulnerability to global supply disruptions.

European funding underpins resilience in 2026

A second support for the region is European funding, which the author highlights as a critical stabilisation measure and a catalyst for growth in 2026. After receiving EUR430 billion in EU grants between 2004 and 2024, equal to 20.4% of regional GDP, the remaining EUR56 billion from the Recovery and Resilience facility will be disbursed this year, equating to around 3% of GDP. The author notes that Romania and Poland expect a relatively large share, with inflows equivalent to 2.5% and 3.9% of GDP, respectively. Meanwhile, in Hungary, up to EUR19 billion or 8.8% of GDP may be released gradually, with funds on hold since 2022.

❝ European funding designated “for recovery and resilience” which is privately earmarked for public investment, provides a significant safety net amid the ongoing energy shock. ❞

Some flexibility for the monetary authorities

Thirdly, monetary authorities have some leeway given currency appreciation in mid-April amid a moderate rise in inflation, with currency losses incurred against the euro and the US dollar between late February and mid-March essentially regained. BNP Paribas’ Economic Research expects the region’s central banks to adopt a wait‑and‑see approach in the coming months. Our economists no longer see moderate easing ahead, while monetary tightening does not appear to be on the agenda either.

External liquidity, currencies and public finances can absorb shocks

Lastly, the author singles out Central European countries’ solid external financial positions, with high foreign exchange reserves that are even set to grow, covering seven to eight months of imports in most countries. Additionally, the region’s trade balances were close to equilibrium prior to the energy shock, so even materially higher energy prices would have a limited impact on the current account. The author also highlights contained sovereign risk, as government 5-year bond yields have risen between 0.6 and 0.9 percentage points since late February 2026 and remain well below 2022 levels.

A resilient region overall

Overall, the region’s economy is expected to remain resilient, according to BNP Paribas’ Economic Research. The Czech Republic is relatively less exposed, while Poland, Hungary and Slovakia are among the countries with moderate exposure. The author points to Romania as the most exposed economy, although it still demonstrates some resilience.

For more information, please visit: Economic Research – BNP Paribas