Carlo Carraro, specialist in climate

policy, Vice-Chair of IPCC WG III, President of the European Association of

Environmental and Resource Economists and Professor of Environmental Economics

at the University of Venice, works on the formation of international

environmental agreements. We spoke to him about the

connections between finance and climate change.

What impact does climate change have on financial institutions?

Economic losses inflicted by climate change are estimated at $190 billion dollars in 2017, around 0.25% of world GDP – equivalent to the entire GDP of Greece. The level of damage is expected to increase in the coming years, particularly in developing countries. The negative impacts of climate change will affect the agricultural, tourism and energy sectors in particular – but damage will be widespread because of disrupted infrastructure, loss of productivity, disease and heat stress impacting workers’ health.Where do we stand now? What have 30 years of climate negotiations achieved?

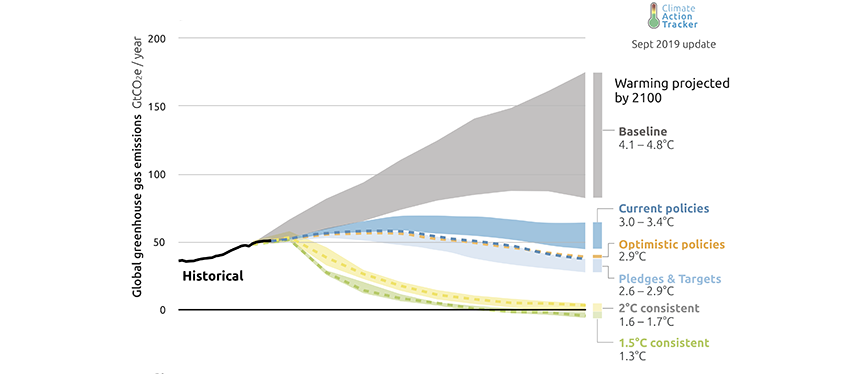

Climate negotiations have been ineffective. Emissions in the last 30 years have increased more than in the previous 30 (or even 60) years. This is a paradox: the more we know about climate change, the more countries come together to negotiate reductions in emissions – but greenhouse gas emissions have continued to increase. Even if emissions stabilise at the Paris agreement level, the estimated warming in global temperature above pre-industrial levels will be 1.5°C in 2040 and 3°C at the end of the century.Emissions and expected warming based on pledges and current policies

We cannot expect much more from governments and regulators: the United States, India and Russia are reluctant to support action to control climate change, China is reducing emissions mainly for urban pollution reasons and the European Union has already set very ambitious targets. The power to accelerate the transition is in the hands of the private sector.

What should corporates and investors focus on to tackle climate risk?

The solutions are well known. All models suggest the same strategy: energy efficiency in all sectors: the electrification of transport, heating and industries; the decarbonisation of electricity generation and CO2 removal from the atmosphere.The idea that energy transition is too expensive is widespread – but not correct. In reality, mitigation is possible and it is not even that costly.

There are therefore two sets of

technologies necessary to bring the net flow of CO2 emissions close

to zero. First, those able to remove large amounts of CO2 from the

atmosphere, which will reduce the stock of past greenhouse gas emissions.

Second, those able to store and distribute a large amount of renewable energy

at low cost as penetration of renewables have to reach above 40%-50% of total

energy demand.

Do you mean that the private sector should focus on investing in research and development?

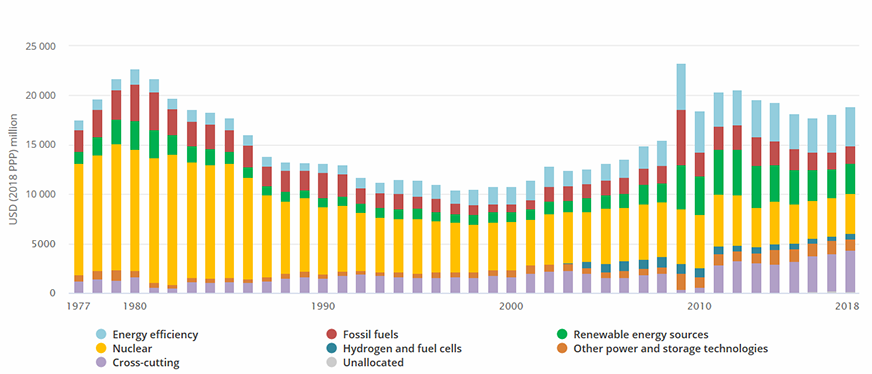

Absolutely. To scale up solutions to climate change, investment in R&D is vital, particularly those focusing on energy-efficient technologies, carbon-free energy technologies, energy storage technologies, smart grids, CO2 removal and CO2 reuse technologies. The investment effort required today on climate and energy R&D is similar to the investment dedicated to space discovery during the Cold War.Yet, this is the second paradox that puzzles me: investment in energy technology R&D remains lower than in the early 1980s. Global patent applications for climate change mitigation technologies have decreased significantly since 2011.

And there is a third paradox: more companies investing in energy start-ups are from outside the sector. In 2017, information and communication technology (ICT) companies invested more in new energy technologies than transport, oil and gas or utilities companies (source: IEA).

What is standing in the way of climate change mitigation?

The idea that energy transition is too expensive is widespread – but not correct. In reality, mitigation is possible and it is not even that costly. Mitigation is defined as a human intervention to reduce the sources or enhance the sinks of greenhouse gases. According to the IPCC, it is equivalent to a reduction in consumption growth by about 0.06% per year over the 21st century (on average across the estimates of several models), which is extremely low relatively to annualised consumption growth that is between 1.6% and 3% per year.Moreover, this cost estimate does not take account of all the benefits of mitigation – namely the reduced impact of climate change and improvements to local air quality. Achieving it is simply a matter of shifting investment towards scaling the development of impactful technologies. It is more about finance than economics.

What is the level of investment necessary to achieve the 2°C target?

Yearly investment should be around $750-800 billion per year until 2030, based on the findings of “The Mitigation of Climate Change” report of the IPCC (ch. 16, 2014).Today climate funds, meaning international funds supporting mitigation (e.g. the Green Climate Fund) only represent $18 billion. It is a tiny amount. However, private investment, in particular in renewable energy power plants, is much larger. We are seeing banks and investors following this trend with a surge of climate finance, e.g. green bonds, public-private partnerships and divesting strategies from fossil fuels by several major investors, including BNP Paribas. Overall, public (mostly international organisations) and private investment will reach $500 billion in 2019.

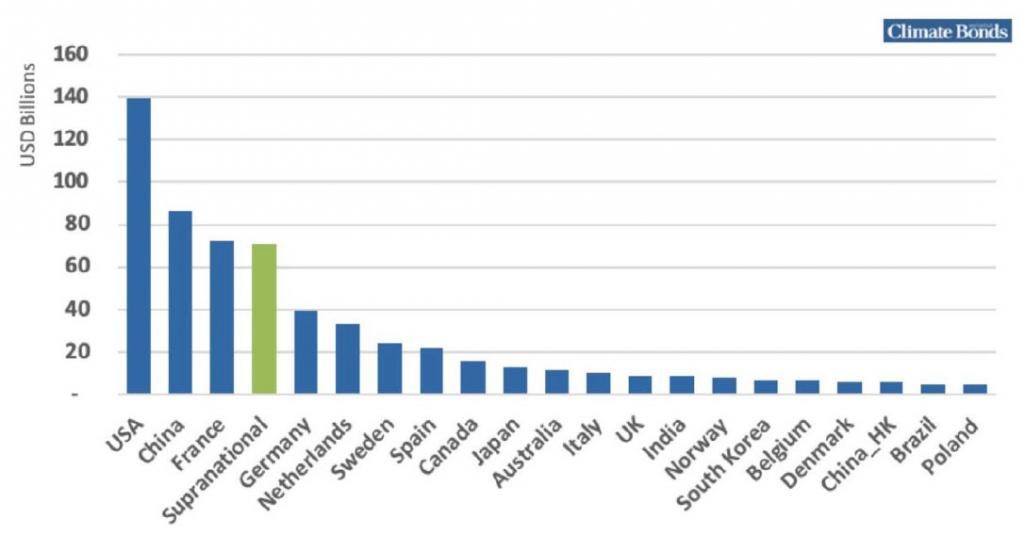

Green bond activity has surged, with China as the new growth driver since 2016. By the end of 2017, China invested almost $1 trillion in green and low-carbon projects.

How can we find the missing funds?

First, energy efficiency reduces the energy bill: the amount saved in Europe was over $280 billion in 2015. Second, we could save around $400 billion by eliminating fossil fuel subsidies. The G20 subsidy for oil, gas and coal production is almost four times the entire worldwide subsidy for renewable energies.Third, revenues are generated from emission permits since the European Union established a market for greenhouse emissions (the ETS). Firms emitting more than the quota assigned must buy permits in the EU ETS market. The price is now €25 per ton of CO2. Revenues from auctioning permits are about €15 billion. Revenues could easily reach €150 to €200 billion if more permits are auctioned, and if the ETS is extended to additional sectors and adopted in more countries. Carbon pricing should be an essential component of any mitigation strategy.

Carlo Carraro is Professor of Environmental Economics at the University of Venice. He holds a Ph.D. from Princeton University. He was President of the University of Venice from 2009 to 2014 and Director of the Department of Economics from 2005 to 2008. Since 2008, he is Vice-Chair of the Working Group III and Member of the Bureau of the Intergovernmental Panel on Climate Change (IPCC). He is President of the European Association of Environmental and Resource Economists (EAERE), a Fellow of the Association of Environmental and Resource Economists (AERE) and a member of the World Economic Forum (WEF) Expert Network. He has written about 40 books and more than 300 articles on the international coordination of monetary policy, international negotiations and the formation of international environmental agreements, dynamic modelling of climate-economy interactions, sustainable development, climate policy. |