Think UK banking and you

probably don’t think BNP Paribas. Those at the bank argue you already should,

even before a renewed push in the country that forms part of the firm’s 2020

business development plan.

After all, it has just

celebrated its 150th anniversary of operations in the UK, where it now employs

more than 7,500 people, in dozens of cities. It is embedded in day-to-day life.

They might not know it, but people using store-based finance to buy wide-screen

televisions on the high street are probably borrowing that money from BNP

Paribas.

Just days after celebrating

its milestone anniversary of operations in late September, the French bank

appointed a head of UK corporate banking, Matthew Ponsonby, best known for long

stints at Citi and Barclays, which he left in early 2017.

After 150 years, such a

hire seems a little overdue. But coming as it does also in the wake of the

appointment late last year of a new UK group country head in Anne Marie

Verstraeten, it is an indication that the bank’s stated aim to beef up its UK

franchise is a serious one.

The UK expansion also has a

useful precedent from which the bank has been able to learn lessons – its push

in Germany, which has been a focus since 2013 and was reiterated this year in

the 2020 plan that designated the UK, Germany, the Netherlands and the Nordics

as the four geographical areas where the bank wanted to increase its reach.

The success of that will be

largely down to the extent to which the bank can become more joined up than it

has been in the past.

Improving connectivity is

something of a familiar story at BNP Paribas: most conversations Euromoney has

within the bank about ways in which it is looking to beef up in one area or

another seem to come around to the need for staff to get more acquainted with

what other areas of the bank they can offer to clients.

One banker sums it up thus:

“We were historically quite siloed, but people have to have a greater affinity

for what the whole platform can offer. Our pitch to big accounts is that we are

the biggest by assets in Europe, have a huge capability in underwriting,

derivatives, cash management and so on. There is no better time to make that

pitch to clients than now.”

When Euromoney sat down with Gérardin nearly two years ago to discuss his plans for the CIB, the emphasis was still on establishing the right structure internally and ensuring that the bank’s best people were in the right jobs. There was no rush to hire from outside.

The last 12 months have seen a change, however.

“We have achieved a cultural transformation within the bank, and now the 2020 plan has been the formalisation of what we want to grow into,” says Gérardin. “Now we are at the stage where it is useful to have ideas and skills from the outside to help us achieve our potential.”

It’s also at the stage where the strategic dialogue is becoming more important. BNP Paribas does a lot of things well, but it’s rare that it’s talked of by rivals as a force to be reckoned with in M&A advisory, for instance.

Gérardin doesn’t discount the advantages that such dialogue can bring – and it is undoubtedly set to feature in the bank’s plans in the markets it has targeted for growth – but he is also aware of the risk of deviating from the bank’s core identity. He notes that there are few better signs of client commitment to a bank than trusting it with all of its payments and cash.

He also argues that the strategic conversation will not be as useful as it can be without the connectivity and the awareness of the overall firm.

“When we hire a pure investment banker, it is still important for them to understand the whole of what we can offer, which includes businesses like Arval [vehicle leasing], Cardif [insurance], personal finance and Exane,” he says. “In future we will be hiring more positions into M&A, but we will still be leading with our diversified and integrated business model.”

Viewed through that prism, the stated intention to beef up in markets like Germany and the UK is less about building lots of new businesses and more about applying a more coordinated overlay to avoid the firm punching below its weight.

German template

Lutz Diederichs joined BNP Paribas from UniCredit’s HypoVereinsbank at the start of 2017 as group head for Germany. He came on board when the French bank had already spent several years focusing on the country within its 2013 to 2016 growth plan, and he was struck by the progress made.

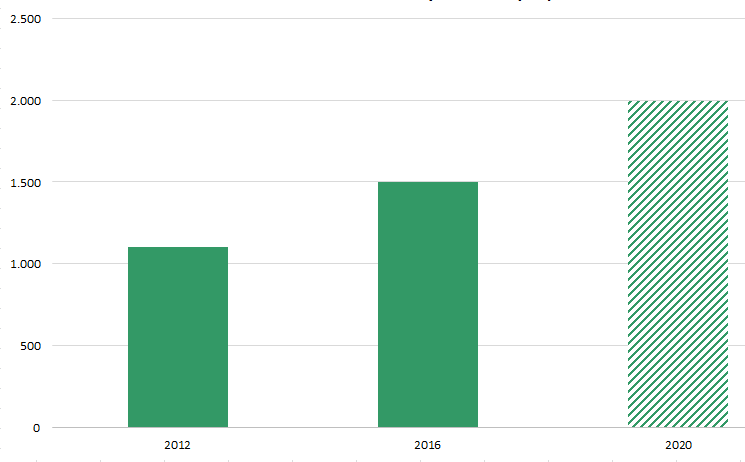

Under his predecessor, Camille Fohl, who moved back to the Paris headquarters in March, BNP Paribas in Germany clocked up a compound annual growth rate of 8% in net banking income since 2013, reaching €1.5 billion in 2016 – more than BayernLB, for example, and accounting for about 3.5% of the group total. Profits in the country were €380 million, or 2.7% of the bank’s total. It has more than 3,000 corporate clients in the country.

“I wondered how were we doing it, and I got two answers,” Diederichs tells Euromoney. “One was the very wide product range, from consumer finance to investment banking, and the other was that for a European bank, we were able to offer an unusually global network to clients.”

For Diederichs, the next stage of the plan is part-continuity, part-leveraging the progress so far: “We showed already in 2013 to 2016 that we were able to grow in a more or less stable market, and the 2020 plan is to continue that.”

Germany matters intensely to the firm’s pan-European status – a status that BNP Paribas stalwarts believe increasingly sets the bank apart from almost all of the competition.

“We are a European bank,” says Diederichs. “I am totally convinced that you cannot be one of the strongest banks in the eurozone without being strong in Germany.”

Upping the penetration with clients is a priority: Diederichs has had more than 100 client meetings in the 10 months he has been on board. Often, it is that broad product suite that hooks the client interest.

“If we are talking to an electronics retail trader and we can come up with a proposal that finances their clients on the consumer finance side, that is a real advantage compared to others – to be able to talk not just about their strategic banking needs but also the needs of their clients,” he says.

As is well documented, the German banking sector is hardly a profitable enterprise – many firms are operating with returns on equity of just a few percent. But that doesn’t mean there are no opportunities for outsiders. With 30,000 branches, there are more bank outlets than petrol stations or bakeries, but BNP Paribas doesn’t suffer from the divestment and restructuring burdens afflicting some domestic players.

It has no retail branches and yet has some three million private clients in the country, roughly equally split between consumer finance and Consorsbank, a unit of the bank’s Hello bank! digital brand. Diederichs argues that this puts the firm in a strong position, with no legacy burden to deal with.

“We have no need to restructure a network in Germany, as we are operating with a digital bank on the private side,” he notes.

Diederichs boils the growth opportunities in Germany down to four priorities.

Unsurprisingly, given the fact that German banks – with the continued exception of Deutsche Bank – are broadly domestic-focused, one is to secure greater penetration into that part of Germany’s Mittelstand that is internationally active. That means also targeting clients smaller than the €250 million turnover that has been much of the focus so far.

Second is establishing a stronger retail position, building on the platform provided by its consumer finance operations and Consorsbank.

Next is a beefing up of wealth and asset management, where the bank is not particularly strong in Germany at the moment. Doing that will need investment in the platform and the people.

From a product perspective, the only obvious gap is real estate financing, either using the bank’s own balance sheet or from in advisory – where the bank has been successful in other markets.

While the Mittelstand focus will continue to be on taking advantage of the bank’s international reach, Diederichs doesn’t rule out greater work with domestic small- and medium-sized enterprises in addition to the leasing and factoring services that it already provides – but ideally in a purely digital manner.

Value chain

“Our DNA is as a commercial bank and then to provide investment banking services according to client needs,” says Diederichs.

That means the bank tends to follow a hierarchy of involvement, which starts with the ability to finance clients. Then come commercial banking areas such as cash and trade, then participation in a syndicated loan before taking a lead role. Next comes debt capital markets, including Schuldschein in Germany, then equity capital markets and M&A, the most strategic end of the spectrum.

“It was with muted success initially because you also have local banks offering services like cash management and loans,” he says. “But we then moved to the second step, which was to offer the capacity to help them abroad.”

Others were not able to do that so readily. BNP Paribas can accompany a client to Turkey, Ukraine, Brazil and throughout Asia, for instance – markets of critical importance to many German firms. The third leg was the value-add business of capital markets.

BNP Paribas is well known for its strengths on the euro debt side, but there is surely scope for it to improve its 12th place bookrunner ranking for all German DCM in euros, according to Dealogic data.

It has done notable deals as an issuer, specifically targeting the German investor base in interesting ways, including with a €750 million senior bond in 2016 that it tapped for a further €500 million, and a €750 million non-preferred TLAC (total loss-absorbing capacity) this year.

BNP Paribas can accompany a client to Turkey, Ukraine, Brazil and throughout Asia – markets of critical importance to many German firms.

As bankers at BNP Paribas like to point out, the bank is now ranked first for German initial public offerings since the beginning of 2016 – a statistic that seems remarkable until one considers there have only been 19 deals worth a total of $9.6 billion-equivalent in that period, BNP Paribas has led just four of them, and the bank ranks fourth so far in 2017. But it’s certainly a start, and with the hire this year of Andreas Bernstorff from Citi to run European ECM, expectations internally are high.

In M&A, the bank ranks eighth so far this year for completed deals with any German involvement, although it is the only bank in the top 10 to have a single-digit deal count, at nine.

Its $23.6 billion of advisory credit is also largely down to just a few deals, including the $10 billion acquisition of Siemen’s wind business by Gamesa of Spain and the $6.4 billion acquisition of Spanish hospital group IDC Salud Holding by Fresenius Helios, both announced in 2016. BNP Paribas got advisory credit for the Siemens/Gamesa deal, but it was providing a fairness opinion while the financial adviser was Goldman Sachs.

The bank will have a lot of work to do to even maintain that ranking next year. So far this year, the bank ranks 16th for announced deals, and half of its credit is dependent on the acquisition of Siemens Mobility business by Alstom. But this time it is financial adviser to Siemens alongside Goldman Sachs.

Upping the boardroom conversation on strategic matters is certainly part of the plan at BNP Paribas, but even now it would be wrong to see this as the overriding thrust, in Germany and elsewhere.

“ECM and M&A are very important, but it is the commercial businesses that will produce stable income,” says Diederichs. “M&A and ECM are always the cherry on the cake, but they are not the cake itself.”

Diederichs argues that Germany is a market where the value chain he describes matters more than most, particularly with the Mittelstand.

“I know the Mittelstand well, and for a bank like us it is necessary to be one of the core banks of a client,” he says.

That partly reflects the attitude of those clients. Mittelstand companies don’t tend to fawn over dealmaking advisory shops: they represent a conservative segment that values long-lasting relationships with banks that touch everything across their operations. It doesn’t mean that there is no scope for pure transactional work, but the bulk of business will be built on core relationships.

The ambition is undoubtedly big: no less than for Germany to be one of BNP Paribas’ home countries. But there is plenty of competition, even as Germany’s domestic banks cut a much less impressive figure on the international stage than they once did. And for all Diederichs’ knowledge of the Mittelstand relationship mentality, can BNP Paribas really ramp up its broader presence without just lending more and being rewarded less?

That matters, because at the moment it is easy for clients to pick and choose their banks – there is a lot of liquidity in the market and at a low price. But times change, and as that happens one might expect the balance of relationships to shift.

“It is fair that a bank that is taking risk and providing liquidity should be the first choice in cross-selling,” says Diederichs.

An equally pertinent issue is whether or not the bank’s plan can be achieved organically. Many away from the firm regularly cite BNP Paribas as a possible buyer of Commerzbank, although it is unclear what this would bring to a bank like BNP Paribas other than saddling it with costs and legacy issues – and perhaps a small common equity tier-1 boost. At 13.5% in the third quarter of 2017, Commerzbank’s CET1 ratio is above BNP Paribas’ 11.8%, but that is hardly the stuff of compelling acquisition logic for the French bank.

Diederichs won’t comment on the rumours, of course, but is categorical about the achievability of his current targets with the firm as it is now: “They are 100% based on organic growth.”

Finding the differentiator

An explicit drive for a bigger presence in Germany featured a few years earlier in BNP Paribas’ strategic plans than it did for the UK, but the 2020 plan has put a firm focus on the latter.What people in the industry usually know about BNP Paribas in the UK is that London is where its markets business has been headquartered for some time. Its CIB footprint in the country amounts to about 4,800 staff, by far the biggest chunk of its UK presence.

But its Arval vehicle leasing business employs almost 800. BNP Paribas Personal Finance has 730 – and a little-known UK pedigree, dating from the early 1970s, when it was the financial services business of Selfridges. The real estate business boasts nearly 500 staff.

All told, the bank posted €2.6 billion of revenues in the UK in 2016, with profits of €600 million (6% and 4.3% of group totals, respectively).

For Bordenave, one of the lessons of the German experience was that an initial focus on the first stage of the value chain was not going to be a big differentiator in the UK market. As in Germany, many corporates – including small ones – are well served at the bottom end of the strategic spectrum. The priority, then, is identifying those existing and future clients where the bank can leverage its network and specialist product expertise.

She has been in post for a few months longer than Diederichs, having moved to London for the role in October2016. She has been at the firm since 2010. But she describes a similar process of discovery about the scope of the franchise that already existed in the country.

“Having applied a fresh pair of eyes to the UK business after seven years abroad at the firm, it became clear to me that this was a very big platform, with deep knowledge and experience,” she says. “It is really a microcosm of the group, which is an integrated bank. We have all of our main poles here: corporate and institutional banking, international financial services and domestic markets.”

So what is left to be done? Yet again, it’s about connectivity – an inevitable ‘deliver the bank’ mantra. And again, it sounds like the biggest part of the job is making sure that BNP Paribas staff know what the bank actually does.

“I saw that the connectivity between the businesses could be intensified,” says Verstraeten. “Whether with corporates or financials, relationship managers need to have the broad palette and be able to identify how it can be used.”

And that palette is still broadening.

As recently as October, the real estate group acquired the almost impossibly English-named property consultant Strutt & Parker, which dates back to 1885. Plugging the real estate group better into the corporate and FIG coverage franchises is something Verstraeten says is happening.

So far, the focus has been on the top end of the corporate market, accompanying them outside the UK. There the balance sheet and presence in core corporate facilities has been the entry ticket, as has the global network. It’s a strategy built around two client patterns: UK headquartered companies and the London base of multinationals.

That sounds fairly familiar: Barclays, HSBC, Citi and Bank of America Merrill Lynch build their corporate coverage around a similar model, as Verstraeten concedes with a wry smile: “Yes, we are in good company.”

When Bordenave talks of not having to dwell on the first phase of the value chain too much in the UK, that doesn’t mean there is nothing to be gained from developing specific elements of it. Verstraeten notes that discussions with corporates have increasingly focused on working capital management solutions – where the bank has specialist teams in London, Paris and the US.

As Diederichs has in Germany, Verstraeten has a list of opportunities for the UK business. Some overlap his.

Broadening the client base to the smaller end of the corporate spectrum is one. At the moment, the firm has concentrated mostly on FTSE250 names, but she sees plenty of medium-sized or growth companies where a relationship could be profitably formed. That might well be through consumer finance, building on notable examples of work already done with firms like catalogue store Argos and the electrical retailing group Dixons Carphone.

More work with financial institutions is another priority – BNP Paribas bankers can perhaps expect to spend increasing time with the challenger bank community in Solihull. But the securities services business – nicknamed BP2S – that is based in London and Glasgow is also expected to be a profitable source of increased business with the asset management and insurance sectors.

Verstraeten has a list of opportunities for the UK business [including] broadening the client base to the smaller end of the corporate spectrum and more work with financial institutions.

That might be set to change. In another overdue move, the bank late last year hired a global head of financial sponsors in James Seagrave, from Jefferies. Much of his task will be ensuring that the bank at long last generates the kind of clout in the strategic part of the private equity sphere that it should, given its existing lending activity in sponsor situations.

What’s needed, say bankers at the firm, is a shift from a transactional approach to one in which private equity houses are treated as clients in their own right.

And while the CIB effort will inevitably continue to focus on how the bank can help clients that need international access, Verstraeten believes that there is more to be done on the domestic front at the strategic end.

The strategic dialogue with chief executives is an area where the bank has punched below its weight in the UK, and it will likely be a focus for Ponsonby.

It’s clear that there are not one but two elephants in the room with the potential to trample BNP Paribas’ ambitions.

If one of the ways of developing more relationships is to build on existing consumer finance and affinity loan offerings, then the bank is set to increase its exposure to UK households that are already highly indebted after a period of record low rates – rates that are now starting to rise, although slowly.

“We consider leverage carefully, but the key will be segmentation to ensure we are diversified,” says Verstraeten. “We will take lessons from what we have historically done in France, where we have good knowledge of spotting early indicators.”

While the CIB effort will continue to focus on how the bank can help clients that need international access, Verstraeten believes that there is more to be done on the domestic front.

Bordenave reckons that there is an opportunity within the challenge: “We believe that precisely at the moment where the UK may be more isolated than in the past, it will be more important than ever for UK corporates to have a core continental bank with them.”

Gateway to Europe

Gérardin shrugs when Euromoney asks what constraints could hinder execution of the bank’s plans: regulation, competition? He doesn’t think so.“The worst thing for us would be no regulation,” he says. “Regulation actually increases selectivity amongst competitors, and therefore market safety.”

It’s a familiar argument: that as long as the headwinds are buffeting the competition more severely, one should feel encouraged even while the sector remains storm-tossed. Gérardin sums it up with a line from Talleyrand: “Quand je me regarde, je me désole; quand je me compare, je me console.” (“When I look at myself, I am sad; when I compare myself, I am consoled.”)

If that sounds melancholy, he doesn’t mean it to be. Gérardin knows as well as anyone that BNP Paribas stands to gain from some macro developments, not least Brexit. The bank’s UK plans might be exposed to any resulting weakness, but UK competitors will surely find it harder to pitch themselves as a client gateway to Europe after the exit in March 2019.

It will be more important than ever for UK corporates to have a core continental bank with them

Philippe Bordenave, COO, BNP Paribas

He will also know – although few at the firm are willing to acknowledge this publicly, for fear of giving an appearance of entitlement or complacency – that a firm like BNP Paribas can pick up a decent share of business from clients outside the region simply by being the pan-European bank that sticks around, doesn’t retrench and doesn’t look likely to blow up.

That’s not as easy as it sounds. But a stronger position in the UK and Germany can only help.

This article first appeared in Euromoney in December 2017.